Military Money Manual has partnered with CardRatings for our coverage of credit card products and may receive a commission from card issuers. This site may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. Some or all of the cards that appear on this site are from advertisers and may impact how and where card products appear on the site. This site does not include all card companies or all available card offers. Editorial Note: Any opinions, analyses, reviews or recommendations expressed in this article are those of the author's alone, and have not been reviewed, approved or otherwise endorsed by any card issuer. Welcome offers vary and you may not be eligible for an offer. All information about the American Express® Green Card, Marriott Bonvoy Bold® Credit Card, and the Chase Freedom Flex® Credit Card has been collected independently by Military Money Manual. These cards are no longer available through CardRatings.com. The information related to the Chase Sapphire Preferred® Card, Chase Sapphire Reserve®, United℠ Explorer Card, United Quest℠ Card, United Club℠ Card, Southwest Rapid Rewards® Priority Credit Card, Southwest Rapid Rewards® Premier Credit Card, Southwest Rapid Rewards® Plus Credit Card, The World of Hyatt Credit Card, IHG One Rewards Premier Credit Card, Marriott Bonvoy Boundless® Credit Card, and Aeroplan® World Elite Mastercard® Credit Card was collected by Military Money Manual and has not been reviewed or provided by the issuer of this product/card. These cards are also no longer available through CardRatings.com. Thank you for supporting my independent, veteran owned site.

One of the most frequent questions I get is: won’t opening all of these cards hurt my credit score?

Short answer: no.

Long answer:

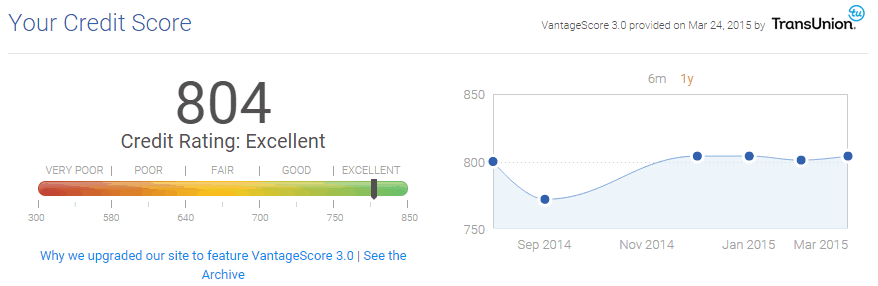

My credit score, as measured by Credit Sesame and Credit Karma, American Express, and Chase has bounced around between 790-830 for the last 10 years. Here’s some proof:

In the last 3 years I have opened 30+ credit cards and closed 7 of the accounts. Still, my score won’t budge from around 800.

I have no other debt, no auto loan, no mortgage, no student loans, no credit card balances. I pay my cards off in full, usually before the statement arrives, so they report a $0 balance. Still, 800+ credit score.

In this post:

How FICO Calculates a Credit Score

FICO isn’t the only credit score in town anymore, they are still the gold standard that 90% of the industry uses.

Many banks and lenders tweak the formula based on their goals and risk management procedures, but the general concept remains the same.

The FICO credit score formula takes into account payment history, amounts owed, length of credit history, new credit applications, and types of credit used.

Payment History (35%)

This one’s simple. Pay your bills on time. Do not miss a single credit card, student loan, mortgage, or auto loan payment. Automatic payments are easy to set up and the computers never forget.

Amounts Owed (30%)

This is known as the “debt-to-income” ratio, or DTI. DTI is a measurement of your monthly payments versus your income. If you make $5000/month and owe $1000 in student loan payments, your DTI is 20%.

Note that this is based on monthly payments, not total amount owed. So if you have a 30 year mortgage, you may owe $100,000s, but your monthly payments are probably still well under your monthly income.

For me, I bought a home that was only twice my annual income. This, plus my student loans and auto loan kept my DTI well below 20% in my 20s.

Now my DTI is 0%, as I carry no debt and pay off my credit cards every statement.

This can also measure your access to credit vs. your credit usage. So if you have a $10,000 credit card, this component measures whether you carry a balance or pay it off every month. I’ve paid mine off every month, so I always have access to much more credit.

Length of Credit History (15%)

This is where you need to start young. If you’re reading this and don’t have any credit, follow my credit card guide for military personnel.

The longer you have a credit line open (like a credit card), the longer your average age of accounts will be. If you have a 1 year old credit card and open up a new auto loan, the average age of your accounts will drop to 6 months.

For myself, I opened a credit card when I was 18 years old. Unfortunately I was not as smart at the time and cancelled that card before reporting to active duty. I should have held on to the card as it had no annual fee.

However, I still have a 9 year old USAA credit card open with USAA that I never use. I just activate it and then cut it up every time they send me a new one.

The account is still open and I charge my biannual auto insurance premiums to the card, ensuring that the card stays open. This increases the average age of my accounts and adds some more weight to my 800+ score.

New Credit (10%)

This can have a negative effect on you if you’ve recently applied for a lot of credit cards. The inquiries will show up on your credit report for about 2 years.

When I had 8 inquires on my credit report (mortgage loan shopping, credit cards, and buying a new car), my score was as low as 740. When the time limit for those inquires expired, my score jumped up 60 points to 800.

Types of Credit Used (10%)

This takes into account whether you have a “good” mix of credit sources, such as a mortgage, home equity loan, auto loan, credit card, etc. This is such a small percentage of your overall score that you can really do just fine with a few credit cards and a mortgage.

Do NOT delay paying off a car loan or credit card just to increase your credit score. This is a dumb money move. You can have an 800+ credit score with only credit cards and no debt. My history is proof of that.

Check your credit score today with Credit Sesame or Credit Karma