Military Money Manual has partnered with CardRatings for our coverage of credit card products and may receive a commission from card issuers. This site may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. Some or all of the cards that appear on this site are from advertisers and may impact how and where card products appear on the site. This site does not include all card companies or all available card offers. Editorial Note: Any opinions, analyses, reviews or recommendations expressed in this article are those of the author’s alone, and have not been reviewed, approved or otherwise endorsed by any card issuer. Welcome offers vary and you may not be eligible for an offer. All information about the American Express Green Card, Marriott Bonvoy Bold Credit Card, and the Chase Freedom Flex has been collected independently by Military Money Manual. These cards are no longer available through CardRatings.com. Thank you for supporting my independent, veteran owned site.

Top recommended military life insurance products:

- Armed Forces Mutual (formerly AAFMAA)

- Navy Mutual

- USAA

Get a quote from all 3 for 20-30 years of term life insurance, usually $1 million is sufficient combined with your $500,000 of SGLI. Don't forget to get a quote for your spouse as well, especially if you rely on his or her income or they are the primary child caregiver.

Podcast episode on military life insurance with Jerry Quinn, CEO of Armed Forces Mutual (formerly AAFMAA):

In this episode, we cover the “DIME-L” framework for deciding how much life insurance you need and the 10x income rule of thumb.

- DIME-L

- Debt – How much debt would need to be repaid if you died?

- Income replacement – How many years of income do you need to cover for dependents?

- Mortgage – Do you want your family to pay off your mortgage?

- Education – Do you want to provide for your children's education?

- Legacy – Do you want to leave an inheritance beyond your current net worth?

- “10x income” rule of thumb

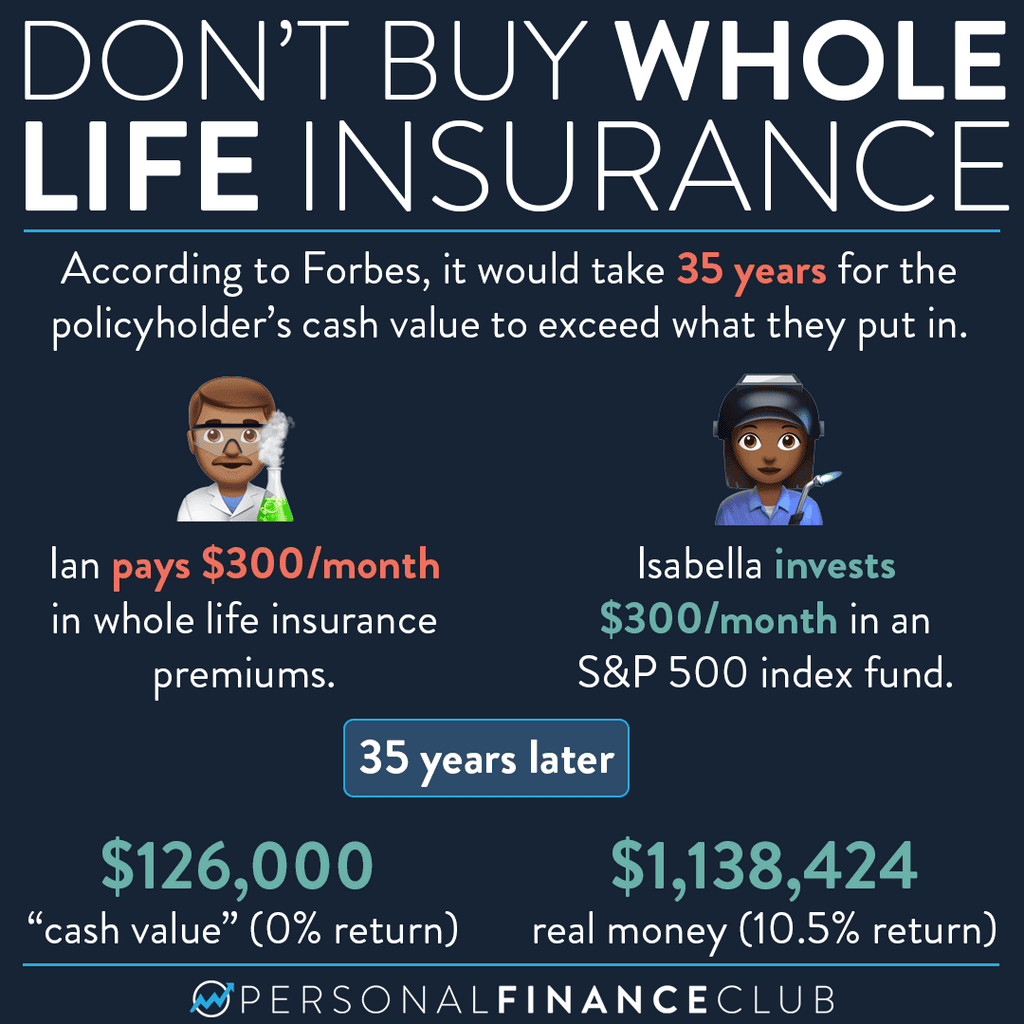

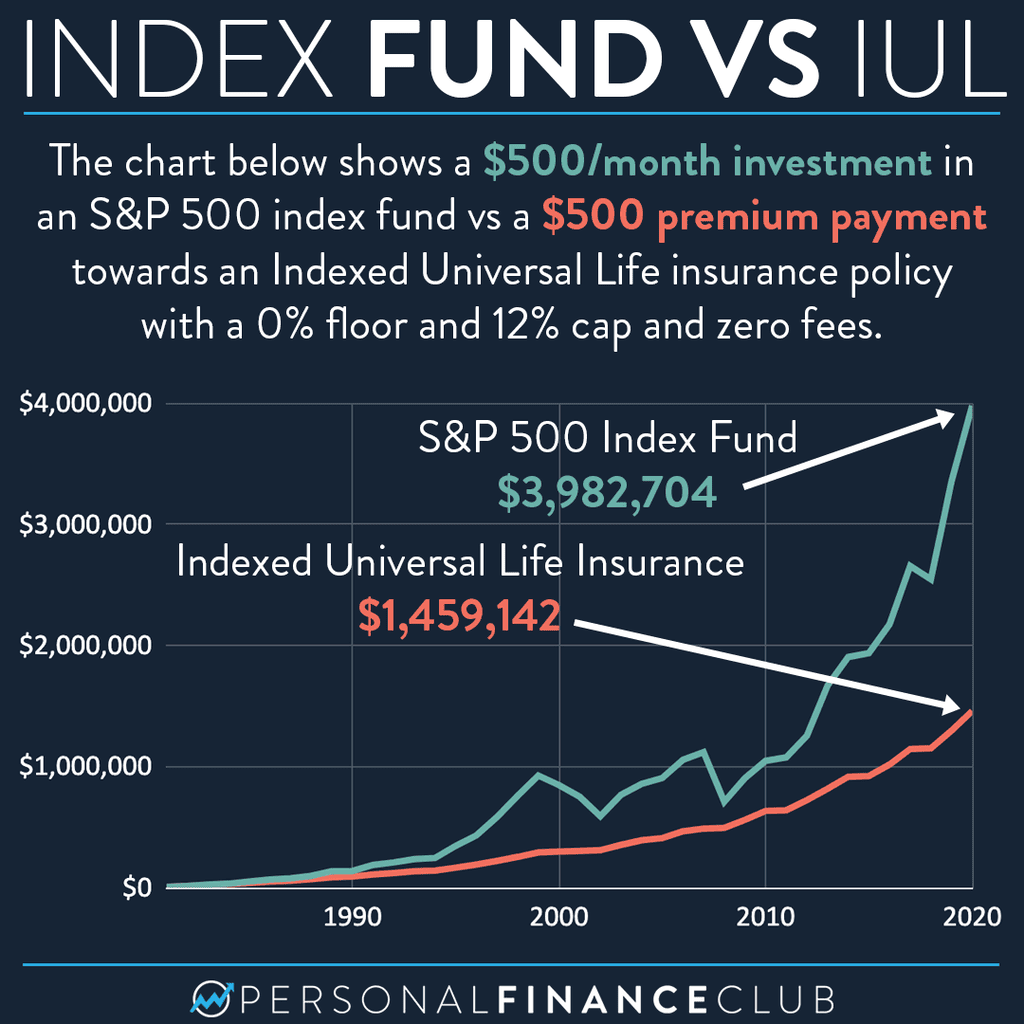

DO NOT talk to anyone trying to sell you whole life insurance, indexed universal life insurance (IUL), or trying to sell you life insurance on your 5 year old child. You can do better than First Command.

In this post:

Life Insurance Background

Life insurance can be one of those things that you don’t want to think about. Contemplating what happens if you were to “buy the farm” isn’t the most fun imaginative exercise. Plus, it’s pretty boring. I almost hate to be writing about it, but it is very important to take a few minutes at some point in your life to ensure that your life insurance is set up the way you want it.

As a military servicemember, you must realize that your job is dangerous and the unexpected can happen, even to young, healthy soldiers, sailors, airmen, or marines. Insuring yourself will help loved ones with expenses in the case of your untimely death and provide some financial security for them in troubling times.

Even if you are single, you should consider low cost life insurance. You can designate anyone you want as a beneficiary, to receive the payment in the case of your premature death. Dying while on military service will automatically generate a $100,000 “death gratuity” to your family to cover funeral expenses.

What to Look for in a Military Life Insurance Policy

Because of the nature of your work, a regular life insurance policy like those available at may not provide adequate coverage for you. Many civilian life insurance policies do not cover aviation accidents, terrorism, or deaths caused by war, which is exactly what you’re trying to insure yourself against.

Make sure that the policy you take out covers you in case you die in war, a terrorism related incident, or an aviation incident. SGLI, Armed Forces Mutual, Navy Mutual, and USAA cover all these clauses. A non-military affiliated insurer may not. Make sure you understand the coverage you're receiving before you start paying for anything.

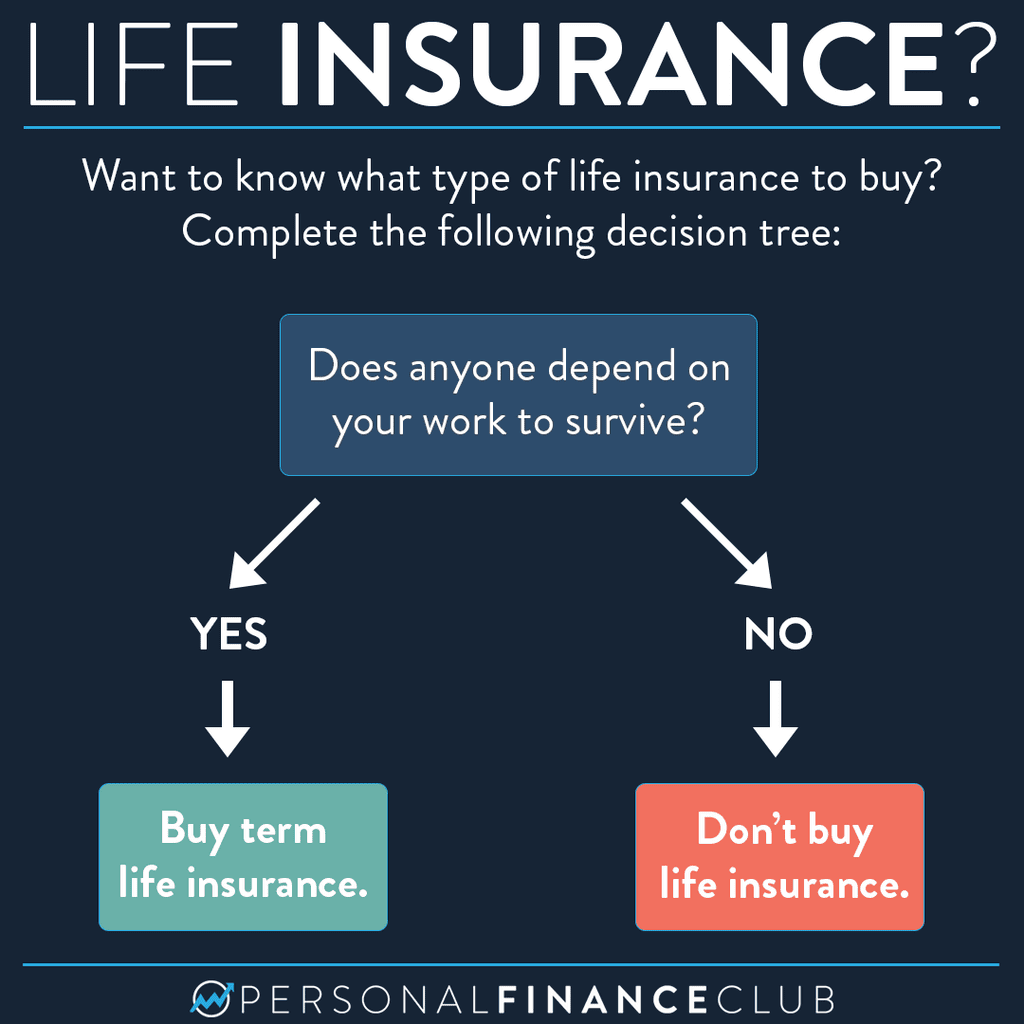

Term Life vs. Whole Life vs. Universal Life

Purchasing life insurance can get tricky in a hurry. There can be lots of confusing terms and you do not want to pay for more than you need.

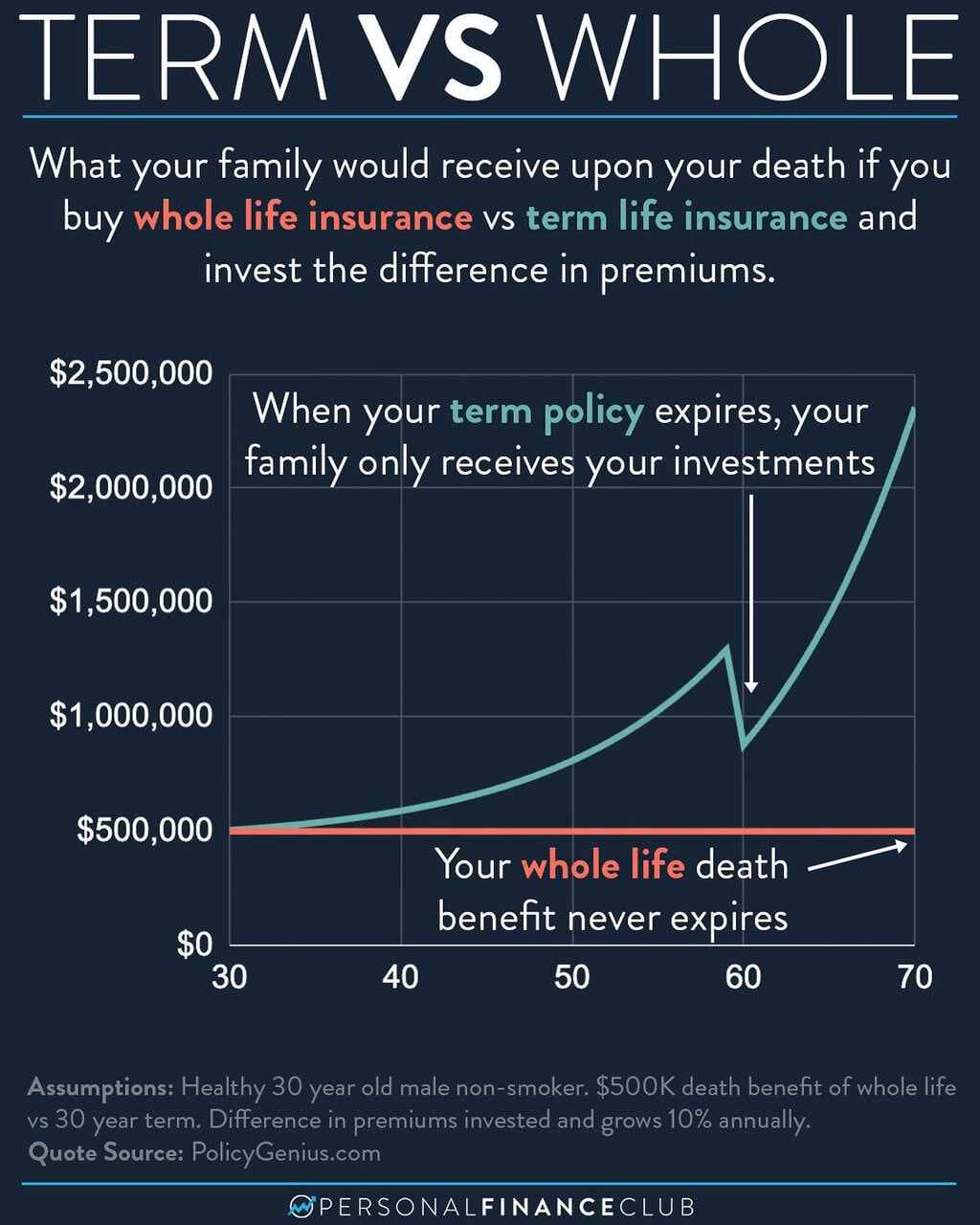

Term life insurance is the simplest and cheapest. It covers you for a set period of time, at a fixed monthly or yearly rate, and pays out to your beneficiaries in the event of your passing. If you are on the path to financial independence, term life insurance is the policy for you. You can efficiently cover yourself until you near financial independence and “self-insure” after that point.

Life insurance is designed to be financial support for your beneficiaries if you were to die early. Once you are financially independent, you’ll no longer need an insurance policy to support your beneficiaries. They’ll be able to live off of the passive income generated by your investments and savings. At that point, you can let your term life insurance expire.

The more expensive, complicated, and unnecessary (at least to the financially independent) life insurance policies are whole life, variable life, and universal life. These “permanent policies” cover you until your death. These policies mix insurance with investments but generally have higher costs and headache involved. They also carry high commissions, so be wary of anyone selling you them.

Cheap Term Life Insurance for Military Personnel

Cheap life insurance is available to most military servicemember’s through the SGLI program. Servicemembers Group Life Insurance (SGLI) is sponsored by the US Department of Veterans Affairs, also known as the VA.

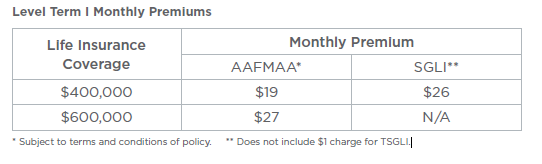

You are automatically enrolled in SGLI as an active duty member of the Uniformed Services. SGLI is provided at 6.5 cents per month per $1,000 of coverage. If you are covered for the full $500,000, you’ll pay $26 per month, plus $1 per month for Traumatic Injury Protection, for a total of $27.

You can insure your spouse (under age 35) for up to $100,000 for only $5 per month under the Family Servicemembers' Group Life Insurance (FSGLI). This, combined with SGLI, can be an easy and cheap way to cover both you and your spouse for only $32 per month.

My wife and I currently use SGLI and FSGLI and have no problem with either program. The cost is deducted directly from the paycheck and SGLI is refunded (free) when you’re in a combat zone. It’s easy to use and probably the only term life insurance I’ll carry while I serve.

Other Low Cost Insurance Options – Armed Forces Mutual, USAA, Navy Mutual

However, your needs may be different. You may want to ensure yourself for more than the $500,000 cap of the SGLI or find a cheaper term policy.

A great organization I’ve found that offers term life insurance cheaper than even the SGLI is AAFMAA, or American Armed Forces Mutual Aid Association. AAFMAA is a not-for-profit, tax-exempt, member-owned association that provides life insurance and survivor services to the U.S. Armed Forces communities. They boast of over 90,000 members and offer some great services besides life insurance.

A quote for a 25 year old Air Force officer who doesn’t smoke was only $19/month for $400,000 of coverage. That’s $8 cheaper than SGLI. Not enough for me to switch from SGLI, but still very competitive and a great supplement to SGLI, if you want that.

AAFMAA also offers coverage for military spouses and for separated servicemembers at very competitive rates. Their idea of putting “members first, always” and their commitment to protecting servicemembers is outstanding. Plus, they’ve been in business for over 130 years. Definitely check them out if you’re interested in life insurance beyond the SGLI. You can compare AAFMAA and SGLI coverage and cost in the chart below:

Navy Mutual also has some great rates and a very solid financial foundation. They can even beat SGLI rates most of the time.

Finally, USAA also offers term life insurance for the US military personnel. While I haven't been able to get a quote (it appears their quote app is broken), USAA typically offers competitive rates to their military members. If anyone has USAA life insurance, I'd love to hear about it.

If you’ve served or are currently serving, who do you use for life insurance? SGLI? AAFMAA? Another company? Is the $500,000 of SGLI enough for you or do you have additional coverage?

Great articles!

One piece of advice I would add to the insurance article is for military members to verify their policy covers them even when serving in the military, aviation (as applicable), etc. I’ve found Navy Mutual Aid to also be a very good option for those reasons.