Military Money Manual has partnered with CardRatings for our coverage of credit card products and may receive a commission from card issuers. This site may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. Some or all of the cards that appear on this site are from advertisers and may impact how and where card products appear on the site. This site does not include all card companies or all available card offers. Editorial Note: Any opinions, analyses, reviews or recommendations expressed in this article are those of the author's alone, and have not been reviewed, approved or otherwise endorsed by any card issuer. Welcome offers vary and you may not be eligible for an offer. All information about the American Express® Green Card, Marriott Bonvoy Bold® Credit Card, and the Chase Freedom Flex® Credit Card has been collected independently by Military Money Manual. These cards are no longer available through CardRatings.com. The information related to the Chase Sapphire Preferred® Card, Chase Sapphire Reserve®, United℠ Explorer Card, United Quest℠ Card, United Club℠ Card, Southwest Rapid Rewards® Priority Credit Card, Southwest Rapid Rewards® Premier Credit Card, Southwest Rapid Rewards® Plus Credit Card, The World of Hyatt Credit Card, IHG One Rewards Premier Credit Card, Marriott Bonvoy Boundless® Credit Card, and Aeroplan® World Elite Mastercard® Credit Card was collected by Military Money Manual and has not been reviewed or provided by the issuer of this product/card. These cards are also no longer available through CardRatings.com. Thank you for supporting my independent, veteran owned site.

If you have a Thrift Savings Plan (TSP) account and separated or retired from the military or government employment, watch out: the “gold IRA” marketers are coming for you!

A poorly written, researched, and presented document called “How Your Thrift Savings Plan is Costing You Money!” surfaced recently from a self-directed “gold IRA” company called “Regal Assets.” I'm sharing it here so you can see for yourself the kind of arguments gold IRA companies make to try to take your money. In this PDF, the company tries to make the argument that rolling over or transferring some or all of your TSP assets to gold makes good financial sense.

Do their arguments hold up? No! Even the most cursory inspection of their arguments reveal that gold IRA companies deal in deceitful marketing practices, engage in fear mongering, cherry pick data, and rely mostly on specious, emotional arguments that do not make sense. Only a confused and fearful simpleton without rudimentary Googling skills would fall for their tricks.

Rather than making you search around to find the answers, I will present some counter-points to their anti-TSP screed. In addition, we will discuss what exactly a gold IRA is and lay out the reasons I do not buy gold.

When any company recommends transferring some or all of your TSP assets out of the TSP, red flags should immediately go up. Especially when gold is involved, caveat emptor: “let the buyer beware.”

In this post:

What is a “gold IRA?”

A gold IRA is a type of a self-directed IRA. Let's talk about what that means.

The IRS defines an IRA as an “Individual Retirement Account.” For the vast majority of US taxpayers, they will open an IRA at a financial institution (known as an account custodian) and invest in traditional financial instruments: shares of companies (stocks), corporate or government debt (bonds), certificates of deposits, money market accounts, etc. My IRAs (Roth and Traditional) are held at Vanguard and are invested like this.

However, a very small number of people decide that the traditional route is not the right one for them. They are special snowflakes and demand a “self-directed IRA.” In a self-directed IRA, you can invest in alternative investments such as:

- real estate

- oil and gas partnerships

- horses

- intellectual property

- precious metals like gold, silver, and platinum.

The IRS specifically prohibits IRA investments in life insurance, artwork, rugs, antiques, metals (other than precious metals), gems, stamps, coins (other than certain coins minted by the US Treasury), alcoholic beverages, and other tangible personal property. IRS regulations also state that a qualified trustee or custodian must hold the IRA assets on behalf of the account holder.

The trustee/custodian provides custody of the assets, processes all transactions, maintains other records pertaining to them, files required IRS reports, issues client statements, helps clients understand the rules and regulations pertaining to certain prohibited transactions, and performs other administrative duties on behalf of the self-directed IRA owner. – Wikipedia

The custodian is there to keep you legal with the IRS. You cannot be your own custodian. Of course the custodian is going to charge you for their unique services, meaning that self-directed IRAs are often very expensive when compared to a Vanguard IRA.

A “gold IRA” is a self-directed IRA custodian that invests primarily in gold and other precious metals. They handle the storage, insurance, and security of physical gold bullion, coins, or bars. There are many companies that offer these services, including Regal Assets, Lear Capital, Rosland Capital, JM Bullion, APMEX, and Goldline.

You may have seen some geriatric actor promoting their gold company of choice on Fox News. All of these companies offer essentially the same services and all are an expensive, illiquid, and complicated way to hold gold in your portfolio.

Is the TSP Costing You Money?

Now that we know what a gold IRA actually is, let's discuss Regal Asset's weak attempt at scaring TSP participants into their self-directed IRA scheme. The title of the 10 page PDF is “How Your Thrift Savings Plan Is Costing You Money!”

Bringing up costs is an interesting tactic to approach the idea of rolling over some or all of your TSP assets into physical gold bullion. The TSP is literally the least expensive 401k-like investment option widely available in the United States and perhaps the world. In the PDF they actually mention this fact:

Its fees are a mere 0.3%, the lowest among all retirement plans.

Actually, this is incorrect, just one of the many facts this PDF gets wrong. TSP fees in 2015 were 2.9 basis points, or 0.029%. That means on $1000 invested, you would only pay $0.29. That's a quarter and a nickel annually per $1000 invested.

Gold IRA companies will charge $250-$360 annually in account management fees along with other fees. You would need a TSP account of $833,000 – $1.2 million to see the same amount of expenses in your TSP account.

Clearly, the gold IRA companies do not have a leg to stand on when it comes to claiming they charge lower fees.

Does Gold Offer Better Returns Than the TSP?

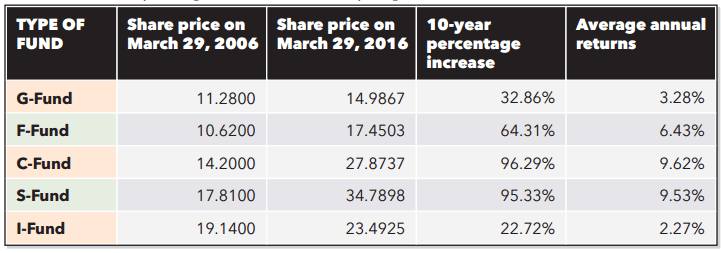

In the next section the PDF presents some data on the returns of the TSP versus gold. The ten year returns of 2006-2016 are presented as somehow disappointing:

The C and S Fund both returned over 9.5% in this time period. Even the bond fund (F Fund) returned 6.43% annualized. Considering the stock market has averaged 6-7% inflation-adjusted annualized returns over the past 140 years, this was a great time to be invested in the TSP! Remember, this time period includes the 2008-2009 recession.

The returns for gold are vaguely presented from 2004-2013. Coincidently, this was one of the best time periods to be invested in gold in the last 20 years. It also conveniently ignores the slightly down to flat performance of gold from Jan 1, 2014 – May 2016 and the 13% drop from Jan 1, 2014-Dec 31, 2015. If there was a time to buy gold, it has probably already passed.

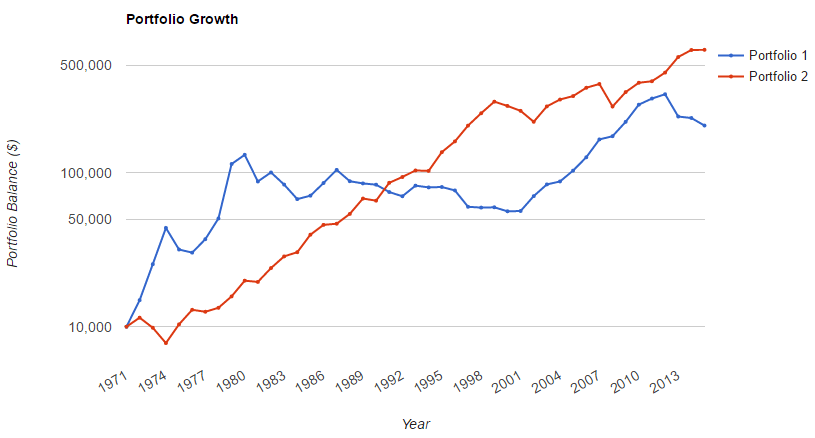

However, there is no way you would have known that in advance. Here's a gold price chart going back 100 years. You can see that in the past hundred years there was no better time to buy gold than in 1971.

Why 1971? That's when President Nixon abolished the US gold standard and moved the US dollar to a purely fiat currency, backed only by the full faith and credit of the US government, and no longer redeemable for gold. So what would have happened if you bought 2, $10,000 portfolios in 1971:

- $10,000 gold in 1971 (shown in blue as portfolio 1) or

- $10,000 of a stock/bond portfolio consisting of 80% total US stock market (VTI or VTSMX) and 20% total US bond market (BND or VBTLX) shown in red as portfolio 2.

Chart generated using the great site Portfolio Visualizer.

Return for the gold: 7.07%. Return for the 80/20 stock/bond portfolio: 9.87%.

Final value of $10,000 invested in 1971: Gold: $202,321. 80/20 portfolio: $628,228. You would be 3 times better off buying an 80/20 stock/bond portfolio than buying gold at the best time in history.

This just further highlights the power of reinvesting dividends and owning thousands of companies that produce the goods and services the world uses. Also, the power of market timing. If you got lucky and bought in 1971, great, you would have done well if you sold at the right time. But you are more likely to buy later and miss most of the initial growth, and sell at exactly the wrong time.

Why I Do Not Buy Gold

My personal investing principles are keeping things simple, low cost, diversified, and automatic. Gold violates all of these principles. When you buy gold, you buy a physical commodity. You are not buying a business like you would with stocks. Gold makes for a terrible investment for several reasons:

- No dividends: half of the returns of the US stock market over the past 100 years have come from dividends. When you buy a commodity, you are not buying a profit generating business, you are simply buying a chunk of metal. Instead of millions of intelligent, hard working people making more money with your money, you own a dust collecting brick.

- Any returns you receive from gold are based on speculation. Since gold is a commodity, its price is set purely by supply and demand. If no one is buying gold, your gold is worthless. Unlike bonds, which generate interest, and real estate, stocks, or other income producing assets, gold produces no income.

- If there was a time to buy gold, it was probably 40 years ago. Gold is the most expensive it has ever been in history. Remember the old saying “buy low, sell high?” Do you think the best time to buy real estate was at the peak in 2006/2007? No!

- Some goldbugs like to make the argument that gold has been a historical means of trade and that if the US/world economy were to collapse or hyperinflation to strike, those holding gold would be the winners in the post-apocalyptic, Mad Max world. However unlikely a scenario that is, don't you think in a postmodern world more useful things like clean water, nonperishable food, medicines, guns, bullets, and oil would be more valuable than a yellow metal with no survival properties? I fail to see any scenario where physical gold becomes the currency of the realm.

- Gold is expensive. It costs a lot to store it, transport it, secure it, and insure it. Even the cheapest way to hold gold (covered below) costs 40 basis points annually (0.40%). That's 13x more expensive than the TSP.

A gold IRA makes even less sense:

- The margins for a gold IRA marketing affiliate are between 1-5%. If they can pay their affiliates that much, how high are the margins for the company selling you the gold? Always question how companies make their money and their incentives for profit.

- Rather than having the gold in your physical possession, the gold is stored at an offsite location. You cannot access the gold physically, which negates any of the doomsday/zombie apocalypse scenarios goldbugs love to bring up.

- Gold IRA companies target senior citizens with deceitful, fear mongering advertising and high pressure sales tactics. They cherry pick data to present a rosy picture of their returns and ignore history and most of Economics 101. They use examples of gold buying in other countries (they especially like to mention “China and India,” the two hottest countries at the moment I guess) to make it seem like you are getting in on some secret. You are not.

Gold is purely a speculative investment that produces no dividends. It represents no ownership in any company and generates no income.

The Best Way to Invest in Gold (If You Must)

Gold is a horrible investment when compared to stocks and bonds over the past 200 years (see chart). If you must in invest in gold, try the exchange traded fund (ETF) GLD. The SPDR Gold Trust ETF holds over $34 billion or 868 tons of gold.

With an expense ratio of 0.40%, this is the cheapest, most liquid, and easiest way to add gold exposure to your portfolio. While it won't be accessible in the event of a zombie apocalypse, we already covered above why physical gold won't help you much in the event of societal collapse.

If anyone ever tells you to withdraw your money from the TSP because they can beat the performance, takea good hard look at their fees. Ninety-nine times out of one hundred it does not make sense to leave the TSP, especially to sink your money into a speculative commodity like gold.

What are your thoughts on investing in gold, reader? I used to hold a bit of GLD in the early 2010s but I realized that it didn't match my investment principles. Do you have any personal experience with a gold IRA company?