Accessing Retirement Accounts Before Age 60

I usually receive one reader question a day through my contact page. I try to respond to all of them. Here’s one of them, lightly edited for clarity, from David: …

Air Force veteran investing for financial independence by age 40.

I usually receive one reader question a day through my contact page. I try to respond to all of them. Here’s one of them, lightly edited for clarity, from David: …

My recent experience with flight cancellation compensation from American Airlines was extremely easy and fast, thanks to some expert help. I received $1003.01 in cash compensation from AA for a …

Earning airline, credit card, and hotel points is a lucrative hobby. You don’t need to travel at all to rack of 100,000s of points through credit card welcome bonuses. Here’s …

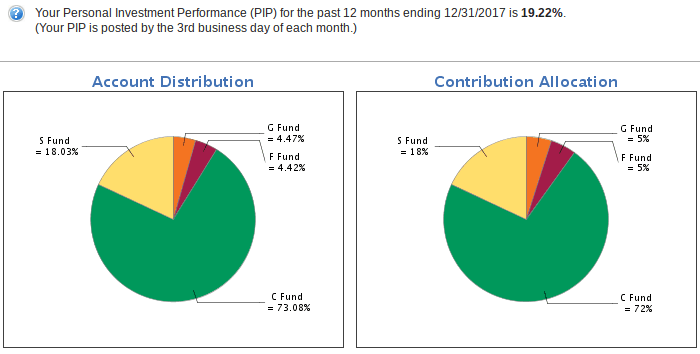

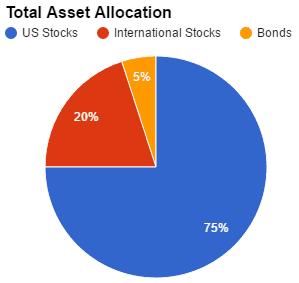

It’s been 2 years since I last posted about my asset allocation. I also wrote about my portfolio in 2014. Let’s take a look again at how my dollars, my …

Oakley, the famous sunglasses manufacturer, has a dedicated division that is committed to serving the specific needs of US military servicemembers, government, law enforcement, rescue, and EMS personnel. The Oakley …

You would think after 10+ years of excellent service I could get around to writing a USAA review. The truth is, this bank makes my financial life so painless, so …

Expires June 30: Get 30% off monthly (for 6 months), annual, or lifetime Aftervault plans! Use this link and coupon code “MMMANUAL” for a 30% off military discount! AfterVault offers …

The following is a guest post from Jason Depew of AviationBull.com. Jason left the Air Force for the airlines after saving a substantial amount of “f*** you” money. He now …

If you opted into the Blended Retirement System (BRS), you should start getting an automatic agency match of 1% and up to an additional 4% agency match. The matching should …

The following is a personal review for Navy Mutual Life Insurance. If you are eligible and get a quote for Navy Mutual Insurance through one of the links below, I …