Military Money Manual has partnered with CardRatings for our coverage of credit card products and may receive a commission from card issuers. This site may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. Some or all of the cards that appear on this site are from advertisers and may impact how and where card products appear on the site. This site does not include all card companies or all available card offers. Editorial Note: Any opinions, analyses, reviews or recommendations expressed in this article are those of the author's alone, and have not been reviewed, approved or otherwise endorsed by any card issuer. Welcome offers vary and you may not be eligible for an offer. All information about the American Express® Green Card, Marriott Bonvoy Bold® Credit Card, and the Chase Freedom Flex® Credit Card has been collected independently by Military Money Manual. These cards are no longer available through CardRatings.com. The information related to the Chase Sapphire Preferred® Card, Chase Sapphire Reserve®, United℠ Explorer Card, United Quest℠ Card, United Club℠ Card, Southwest Rapid Rewards® Priority Credit Card, Southwest Rapid Rewards® Premier Credit Card, Southwest Rapid Rewards® Plus Credit Card, The World of Hyatt Credit Card, IHG One Rewards Premier Credit Card, Marriott Bonvoy Boundless® Credit Card, and Aeroplan® World Elite Mastercard® Credit Card was collected by Military Money Manual and has not been reviewed or provided by the issuer of this product/card. These cards are also no longer available through CardRatings.com. Thank you for supporting my independent, veteran owned site.

The Savings Deposit Program or SDP offers deployed military servicemembers a 10% guaranteed return on up to $10,000 of invested cash. This means you can earn up to $1,000 per year in interest while you are deployed.

I have used the program 3 times over as many deployments. My longest SDP was from July 2017 to October 2019, when I earned over $2,067 on a $10,000 initial investment.

The Department of Defense Savings Deposit Program (SDP) is a special program set up by the DoD to “provide members of the uniformed services serving in designated combat zones the opportunity to build their financial savings.”

Here is great SDP calculator from Garrison Ledger.

In this post:

How The Savings Deposit Program Works

While deployed in a designated Combat Zone Tax Exclusion area, go to any military finance office after you've been in the CZTE (Combat Zone Tax Exclusion areas) for 30 days and fill out the required paperwork to make your deposit.

You can usually make deposits with your Eagle Cash Card, a check, or set up allotments to come out of your pay every paycheck. Usually the finance personnel will unlock your Eagle Cash card so you can add $10,000 to it for a limited period of time to quickly make the transfer from your checking account to the SDP.

Any money in the account between the 1st and 10th of the month is eligible to collect interest, at a rate of 2.5% per quarter or 10% per year. So if you were to deposit $5000 on 15 May, it wouldn't collect any interest for the month of May, but would start collecting in June.

You may deposit any amount you wish into the SDP, but only the first $10,000 will collect interest. If you have $10,000 in the SDP, you can elect to have quarterly payments made to you. This would mean an extra $250 every 3 months. Sweet!

The money will remain in your SDP and continue to collect interest for up to 90 days after you return from a combat zone. Another free $250! At any time you can withdraw some or all of the funds. After 120 days after departing the combat zone, the money will be automatically withdrawn and deposited back in your account linked to myPay, along with an interest accrued.

With $10,000 invested in the SDP, that's $1000 a year in interest from a federally insured deposit program. No one else in the world has access to a guaranteed return like this.

How the SDP Works in Reality

The SDP is an incredible opportunity for service members to boost their investment income. However, there are a couple of caveats to the program:

Unless you get your commander's signature, you can only deposit the amount of you were paid since your first day in country. So if you are deployed for 30 days and only had total entitlements of $4000, you can only deposit $4000 at the 30 day mark. You can later top off the SDP to the full $10,000 throughout the course of your deployment.

As long as you continue to return to the CZTE for at least 1 day every 90 days, your clock resets. This is very beneficial for aircrew or military members who frequently transit combat zones. I have heard of some Air Force pilots who have kept their SDP going for 3 years, before the system finally made them take the money out and redeposit it!

The interest on your SDP is taxed at the normal dividend and interest rate for your tax bracket. Unlike much of your combat zone pay, you have to pay federal taxes on your SDP. Still though, an awesome deal, especially if you're already contributing to your Roth TSP and getting your money into there tax free.

Use the SDP as an Emergency Fund

On a previous deployment, I maxed out my SDP with the full $10,000 in the course of 60 days. I deposited $6000 at my 30 day deployed mark and the additional $4000 at the 60 day point. Depending on your pay and expenses, this may be more difficult.

If possible, deploy with the $10k ready to deposit and increase your TSP contributions to get the maximum amount into your Roth TSP for the year.

The SDP allows you to earn a great risk free return on your emergency fund savings, which were sitting in a low interest rate savings account. SDP funds can be withdrawn within a few days through a simple online form and direct deposited into your checking or savings account. Because of this flexibility, I believe you can utilize your SDP as a way to pump up your emergency fund return while still maintaining quick access to your e-funds.

Always make sure you have at least 1-2 months of cash in a savings or checking account for unexpected expenses. If you're comfortable with your level of instant access cash, investing the rest of your emergency fund money into a safe, easily accessible investment, like a CD or SDP, can be a great way to boost your emergency fund return.

I recommend most military servicemembers use the SDP to invest their emergency fund while deployed in a tax free combat zone.

The SDP is an amazing opportunity for servicemembers to put their hard earned pay to work. You can save an enormous amount of money while you're deployed. Why not get a guaranteed 10% return on those savings?

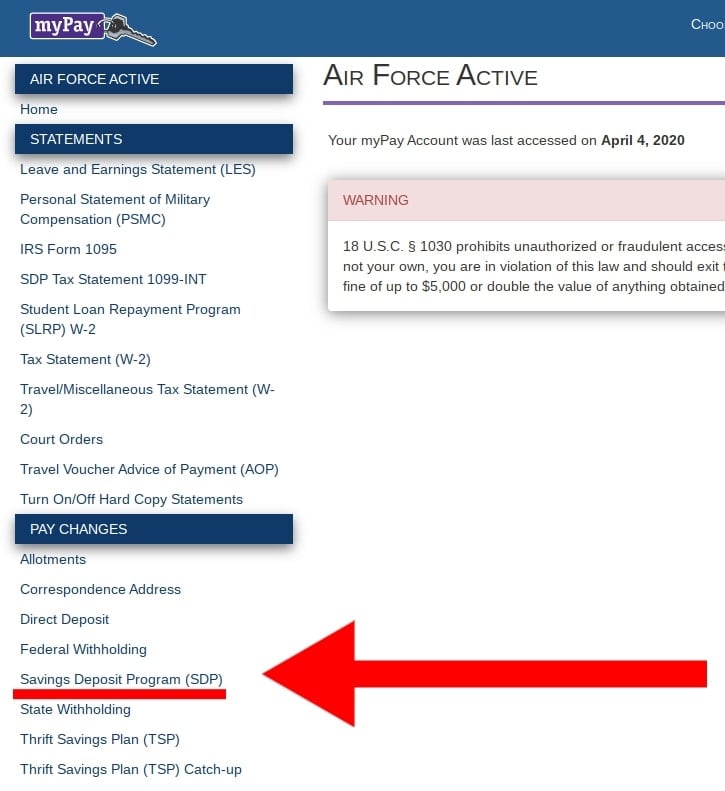

How to Access Your SDP Statement

To withdraw from your SDP or check your statement, you can log on to myPay. You will find the “Savings Deposit Program (SDP)” option on the left side or under the menu in the “Pay Changes” section

SDP FAQ

100% yes! The Savings Deposit Program is definitely worth your time to set up while you are on deployment. Even if you are only deployed for 3 months, you can fund the account after 30 days of being deployed. Then the interest will accumulate over the next 2 months you are deployed and will continue to accumulate for up to 120 days after you return from deployment. If you invest the full $10,000 after 30 days, you should be able to earn $416 in interest over the 5 months you have the SDP invested.

An SDP withdrawal only takes a few days. The one time I needed to pull the cash out quickly it was in my bank account 3 days after initiating the withdrawal on myPay. The SDP makes a good emergency fund.

The SDP allows members of the military to deposit up to $10,000 into a special U.S. Treasury account. Any funds deposited in this account receive 10% interest, paid monthly. For instance you deposite $10,000, you would receive $83.33 per month for the length of your combat zone deployment and 120 days after.

Yes, the income from the SDP will be reported on a 1099-INT in the year the withdrawal is made. For example, if you deposited the money in 2018, stay deployed for all of 2019, and leave the combat zone in January 2020, your SDP account automatically closes 120 days later in May 2020. You will receive a 1099-INT in myPay for the 2020 tax year.

As of 2020, the IRS and DOD designated the following countries CZTE or combat zone tax exclusion areas: Afghanistan, Djibouti, Egypt (Sinai peninsula), Iraq, Kuwait, Saudi Arabia, Oman, Bahrain, Qatar, Jordan, Kyrgyzstan, Lebonan, Pakistan, Somalia, Syria, Tajikistan, Uzbekistan, United Arab Emirates, Yemen. Also the Persian Gulf, the Red Sea, the Gulf of Oman

part of the Arabian Sea, and the Gulf of Aden. Serbia, Montenegro, Albania, Kosovo, the Adriatic sea, and the Lonian Sea north of the 39th parallel are also tax free thanks to an executive order in 1999 that has never been rescinded.

Trying to max my tsp contributions ~72k while I’m there which severely eats into the amount I can contribute to sdp. What’s the process exactly for commander signature? If I set aside $10k in a HYSA for this, can I just move it over when I get out there?

It does compound quarterly, so wouldn’t it technically be up to 1,038.13 for 12 months?

It’s a maximum return of 10% on $10,000. It does not compound on any amount over $10,000. So $1,000 per 12 months or $83.33 per month.

I don’t know if this varies on deployed location but your not allowed to contribute a full months worth of pay until the 61ST day after you’ve been in the deployed area. So for example, if you landed in your deployed location on Jan 1st, you’d have to wait until Mar 1st to contribute an ENTIRE months’ worth of entitlements. Just found out about this at Qatar after trying to contribute an entire LES to the SDP on my 31st day here.

I love the SDP! Where else can you guaranteed returns like this with zero risk. I have used it multiple times through my career. Normally I will do multiple shorter deployment throughout the year which allows me to earn interest for much longer than normal.