Military Money Manual has partnered with CardRatings for our coverage of credit card products and may receive a commission from card issuers. This site may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. Some or all of the cards that appear on this site are from advertisers and may impact how and where card products appear on the site. This site does not include all card companies or all available card offers. Editorial Note: Any opinions, analyses, reviews or recommendations expressed in this article are those of the author's alone, and have not been reviewed, approved or otherwise endorsed by any card issuer. Welcome offers vary and you may not be eligible for an offer. All information about the American Express® Green Card, Marriott Bonvoy Bold® Credit Card, and the Chase Freedom Flex® Credit Card has been collected independently by Military Money Manual. These cards are no longer available through CardRatings.com. The information related to the Chase Sapphire Preferred® Card, Chase Sapphire Reserve®, United℠ Explorer Card, United Quest℠ Card, United Club℠ Card, Southwest Rapid Rewards® Priority Credit Card, Southwest Rapid Rewards® Premier Credit Card, Southwest Rapid Rewards® Plus Credit Card, The World of Hyatt Credit Card, IHG One Rewards Premier Credit Card, Marriott Bonvoy Boundless® Credit Card, and Aeroplan® World Elite Mastercard® Credit Card was collected by Military Money Manual and has not been reviewed or provided by the issuer of this product/card. These cards are also no longer available through CardRatings.com. Thank you for supporting my independent, veteran owned site.

Update 18 Feb 2024: Some people are reporting in the comments that they are falling between the cracks of SCRA and MLA.

Most of the issues have been resolved now as issues on the MLA database and in the DEERS database, especially for military dependents (spouses).

I recommend you first confirm that your Social Security Number is correct in DEERS and you are in fact in the MLA database here: https://mla.dmdc.osd.mil/ . If both of those are correct, leave a comment below and I will see what I can do to help.

Reader “RD” reports in the comments:

Update with success, I called and explained my situation. Guy sent a request to check if I was eligible for SCRA or MLA. Apparently there is a way for them to do that internally. 6 Weeks later they said I was eligible for MLA, sent an update cardmember agreement showing me as a covered borrower, and they refunded the annual fee.

If Amex charges you an annual fee and you are active duty military, please leave a comment with:

- The day you applied for the account.

- The card you applied for.

- Whether you are listed as active duty in the MLA database here: https://mla.dmdc.osd.mil/

- Are you listed as a covered borrower on your account agreement on the Amex card?

- Was the annual fee charged? How long after opening the account?

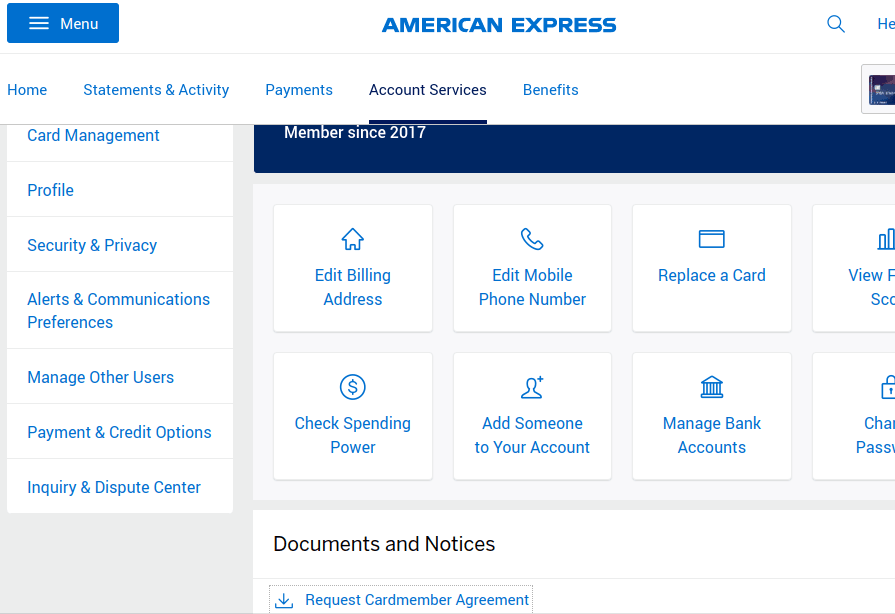

To see if you are a covered borrower:

- Go to your Amex Account Services page.

- At the bottom there is a link to “Request Cardmember Agreement”

- In the agreement you should see the text: “You have been identified as a ‘Covered Borrower’ under Military Lending Act.” on the bottom of page 2.

I would keep insisting to the Amex reps that your account should be handled as a covered borrower.

This is very frustrating as it does not appear Amex customer service reps understand their own MLA and SCRA policies.

I’m sorry this isn’t working on one of your accounts. Please keep us updated if you find a solution.

Update 29 January 2020: This issue appears to have been resolved! Your SCRA request with Amex will be denied if the card is opened after active duty start date. However, this is fine as your account will automatically be enrolled in Amex's Military Lending Act (MLA) program.

Amex credit cards will continue to have special protections applied, regardless of when they open the account. If you open the card account before active duty, SCRA will apply. If you open the account while on active duty or married to a servicemember, MLA applies.

See official statement from one of my sources at American Express. My top recommended card for military servicemembers and spouses is the Platinum Card® from American Express.

We have not changed the relief we provide to our eligible military servicemembers under SCRA and MLA.

SCRA relief covers loans or Cards opened prior to active duty, while MLA relief covers loans or Cards opened while on active duty.

Typically if a Card Members’ loan or Card is ineligible for SCRA relief because it was opened while on active duty they will be notified accordingly and then automatically receive MLA relief instead.

We are happy to assist any military servicemembers on how best to manage their Amex membership prior to active duty, while on active duty, or upon coming home from active duty and into civilian life. We thank them for their membership and service to our country

MilitaryMoneyManual.com source at American Express

American Express now has the Military Lending Act and Servicemembers Civil Relief Act programs.

The Amex program for accounts opened while on active duty is Military Lending Act or MLA.

The Amex program for accounts opened before active duty is Servicemembers Civil Relief Act or SCRA.

Amex MLA

If you open a card while on active duty military or while married to an active duty military servicemember, Military Lending Act (MLA) benefits will be applied to your account.

Your card account will have a note at the top that says: “Account enrolled in Military Lending Act” Any customer service agent on the phone or over chat should be able to confirm this with you. You will NOT receive a letter in the mail.

Amex SCRA

If you open an account before joining active duty, SCRA benefits will be applied to your account. You can fill out the Amex SCRA application here.

You will receive a letter in the mail or emailed to you stating your account is now being handled in accordance with SCRA.

Background on Amex SCRA Denials

In January 2020, many reports came in on Reddit and to my email inbox that American Express changed their Servicemembers Civil Relief Act (SCRA) benefits for military servicemembers.

Go here for an explanation of American Express's new Military Lending Act policy.

The letter or email military servicemembers are receiving looks like this:

To support the men and women who serve in the United States Armed Forces, we are handling your account referenced above in accordance with the Servicemembers Civil Relief Act.

The Servicemembers Civil Relief Act provides for a maximum annual interest rate of 6% per year on loans you received before starting active military duty. Our records indicate your account was opened during the active duty time period. Therefore, this account is not eligible for relief under the Servicemembers Civil Relief Act.

This completes our review of this account. If there are any additional accounts you would like reviewed for Servicemembers Civil Relief Act benefits, please call us at 1-800-253-1720. If you are outside the United States, please call us collect at 1-336-393-1111.

We are grateful for the service and devotion you have shown to our country. Sincerely, American Express Customer Care

The key line is in bold above: “Our records indicate your account was opened during the active duty time period. Therefore, this account is not eligible for relief under the Servicemembers Civil Relief Act.”

What Amex failed to communicate to eligible servicemembers is that while SCRA does not apply, MLA does.

American Express Adding MLA With SCRA

Multiple Amex customer service reps and contacts confirmed special protections will continue under Amex's new Military Lending Act policy.

The Military Lending Act or MLA is an even stronger version of the SCRA. Chase implements their MLA policy in September 2017.

The Chase Military Lending Act program reduces fees on all Chase personal credit cards for US military servicemembers and their spouses. Some of the awesome Chase military credit cards include:

card_name

Learn how to apply on our partner's secure site

- $795 annual fee (see Chase policy)

- bonus_miles_full

- Earn 8x points on all purchases through Chase Travel℠ including The Edit℠

- 4x points on flights and hotels booked direct

- 3x points on dining worldwide

- 1x points on all other purchases

- Get a $300 annual travel credit as reimbursement for travel purchases charged to your card each account anniversary year.

- Live the lounge life at over 1,300 airport lounges worldwide with a complimentary Priority Pass™ Select membership, plus every Chase Sapphire Lounge® by The Club with two guests.

- Up to $120 towards Global Entry, NEXUS, or TSA PreCheck® every 4 years which saves you a ton of time

- Up to $150 in statement credits every six months for a maximum of $300 annually for dining at restaurants that are part of Sapphire Reserve Exclusive Tables.

- Trip Cancellation/Interruption Insurance, Auto Rental Coverage, Lost Luggage Insurance, no foreign transaction fees, and more.

- Get complimentary subscriptions to Apple TV and Apple Music for a minimum of one year when activated by June 22, 2027, a value of $288 annually.

- Member FDIC

- Learn more in the Chase Sapphire Reserve® review

You can also compare the Chase Sapphire Reserve vs the Platinum Card® from American Express card. Both cards have an annual fee and compliment each other when it comes to earning 2 different flavors of flexible reward points.

I also recommend comparing the Chase Sapphire Reserve vs. the Chase Sapphire Preferred® Card.

Amex SCRA Denials Frequently Asked Questions

As of 24 January 2020, there has been no official statement from Amex on why they changed their military SCRA policy. I will update this page as more information comes out.

After contacting Amex customer service reps, it appears that AMEX is shifting away from SCRA to MLA. Before Jan 2020 Amex used to use the SCRA law to apply military annual fee benefits for cards opened while on active duty service. Now it appears they will continue to reduce annual fees for military, just changing the program to MLA away from SCRA.

Military Lending Act benefits are automatically applied to your account when you open the account on active duty. Amex customer service reps should see “Account enrolled in Military Lending Act” as the first note on your account when they pull it up over secure chat or on the phone.

There are no reports as of 24 Jan 2020 that anyone with an SCRA fee benefit already in place has been charged an annual fee. This policy appears to only effect cards that were opened in Dec 2019 or Jan 2020.

If you have any additional information or data points, please share them in the comments. Thank you!

I have 2 data points here regarding SCRA (not MLA) benefits for Amex Business cards. Two of American Express Delta Gold Business Card opened before active duty were approved for SCRA benefits. Here is the confirmation from Amex

“…The Servicemembers Civil Relief Act provides for a maximum annual interest rate of 6% per year on loans you received before starting active military duty. As of today, your account does not have a balance owed which generates interest charges so there is no eligible balance. However, we will not charge the following fees on your account statement for the duration of your active military duty:

Annual Membership Fees

Late Payment Fees

Return Payment Fees

Return ATM Fees

Statement Copy Request Fees

Reactivation Fees

Delivery Rush Fees”

Great data point, thank you. Are you Guard or Reserve? Or you just opened Amex Delta Business before you entered active duty?

Were the annual fees charged?

I have had issues with my Schwab Platinum and Gold (now upgraded to Platinum) that I acquired before becoming an active-duty spouse getting benefits. All the annual fees have hit. Any suggestions? I’ve called to get applied. I’ve also filled out the SCRA application and was denied (but MLA not applied).

Since these issues, I HAVE applied for a new card and MLA benefit was applied automatically.

Hello! I also can’t get the fee waved for my Amex. I’m active duty spouse and I’m in DEERS but somehow not in MLA database.

All the info is correct in DEERS. What can I do to add myself to the MLA database? Do you have any suggestions?

Customer Data or Certificate Questions: For questions related to DEERS data, the information on MLA certificates, a service member’s or dependent’s status, or military service contacts, please call the DMDC Contact Center Tier 1 Web Services 1-800-368-3665.

It might help to have the DEERS people on base call the DMDC MLA people to explain the issue.

I had an AMEX Platinum before marrying my husband, who is active duty. After we were married, my fee was to be charged a month later. I am in the MLA system and in DEERS. My husband is an authorized user. I’ve been charged the annual fee and not reimbursed. I’ve applied for MLA multiple times and been denied, although when I search myself it shows i’m eligible. I’m reapplying for SCRA now trying to get waived under that, but they’ve told me multiple times I wouldn’t be covered. Any insight?

Usually you must be eligible for MLA when you open the line of credit. I would close the account and apply for a new Amex Platinum card. You probably won’t get the welcome bonus again, but at least you’ll get the annual fee waived if you’re in the mood MLA database.

Dang. Or do you think if I open up another account for a Gold card, then it would apply for that card?

Thanks so much for your help!

Yes, if you opened up an Amex Gold card it should apply as long as you’re in the MLA database.

I’ve been having trouble getting approved for my MLA benefit for AMEX platinum acct. Story is –

I am in the reserves. I was put on active duty orders from Mar 2021 to Mar 2022. (back on reserve now).

In Nov 2021, I applied for the AMEX platinum.

Since I opened the account after I was already on active duty, I should’ve been automatically enrolled to MLA.

However, month after opening the account, I was charged the annual fee, NOT followed by the reimbursement.

Since then, I’ve been on numerous calls with AMEX who keep telling me that I am not eligible for MLA. I’ve sent in a copy of my orders for the active duty orders I was on, and a copy of my DD214. I’ve contacted DEERS to make sure my information was also correct.

AMEX continues to tell me that I don’t and didn’t qualify for MLA and I was told that the only thing I can do at this point is call DOD to fix the issue on my profile and then re-do this process.

Escalating this issue with AMEX hasn’t helped, talking to the person who’s the ‘highest level dealing with military accounts’ cannot even recognize what the military Orders or DD214 looks like, let alone comprehend it.

I don’t know what else to do, when I told AMEX that I only opened an AMEX account because I knew I qualified for MLA and the annual fee was to be waived, they said they can offer a $400 reimbursement with a $4k purchase in the next 3months. This is NOT what I am looking for!

Apply for Amex SCRA benefits here.

Not sure if my initial post went through so trying again. Read through most of the posts and in a similar situation as some. Applied while on active duty over the summer and have been denied MLA. No help with AMEX reps, any advice for me to get the fee waived would be appreciated.

Were you in the MLA database?

Not in there now, AD ended in July.

But were you at the time? That’s going to determine if they waive the annual fees or not. If you don’t know, there’s not much you can do. If you go active duty again, you can apply for SCRA benefits and get your fees refunded like others have described.

From looking through the MLA handbook, it looked like it was only going to pull up current AD. I didn’t see a way to back date it for 1.5 months ago?? I also tried the single record request which I was not on since it’s for AD within the last 30 days.

I do not believe there is any way to backdate the MLA database search. I recommend keeping records next time and applying for SCRA benefits as soon as you are showing up in the SCRA database. If you aren’t in the SCRA database after a few weeks of active duty, contact your S1, personnelists, or equivalent for your branch ASAP.

Update: After submitting my orders, SCRA was applied to my account.

I have had the Platinum for 5-6 years and just tried to add Gold. The Platinum is somehow listed as SCRA even though I got it after going on AD. The Gold was denied SCRA but automatically added with MLA. However; the agent I spoke with claims Gold will incur a fee because you can only have “one card that earns membership points”. I’m going to see id they actually charge a fee on the Gold.

The Platinum is SCRA because that’s how Amex marked accounts 5-6 years ago, even if you were on active duty. MLA didn’t come into effect until 2018. The agent you spoke to is not up to speed on Amex military policies. Usually the customer service reps are not familiar with Amex military policies. You shouldn’t have the fee charged on the Gold. Let me know if you do.

Did you add the Gold as an additional card or did you open up a separate Amex Gold card?

I’m a military spouse and applied for Delta Reserve as a primary holder 2 months ago. Amex denied MLA and I got charged an annual fee even though I already have a Gold and a platinum card as an authorised user under my husband’s name and my fees have been waived. I’m not identified as a covered borrower but I’m definitely on DEERS. My husband called DMDC and they said MLA database only shows whether you’re an active duty or not and it doesn’t work for spouses and dependants. We called Amex and applied for MLA so many times but we haven’t got any luck. Also they weren’t 100% sure if adding my husband as an authorised user would trigger the reimbursement. We tried it a week ago and I applied for MLA again. If I get rejected again, I might just cancel the card… :/

That is incorrect. The MLA database does contain information on military spouses as “covered borrowers.” I just pulled the information for my wife, who is a civilian. Here is what the MLA database reported:

There must be something wrong with your DEERS information or DEERS is not pushing to the MLA database correctly. Check birthday, Social Security Number, maiden name, last name – confirm all the details are correct.

Military spouses DO get their annual fees waived with MLA. This has been confirmed thousands of times. There must be something wrong with your account.

Also the DMDC people who answered the phone are wrong as well. The MLA database reports covered borrowers. Covered borrowers are active duty servicemembers OR their dependent spouses. Look at the user guide for the MLA database to confirm this.

I’m sorry for the late reply. So, I found out that my SSN had never been on DEERS.. We updated and now I’m officially identified on DMDC. I applied for MLA a week ago but I haven’t heard back from them. I’ll wait a little more.

Thanks for the update!

If my wife opened a Amex gold card before she got married to me – an active duty member – will the MLA cover her and she will not have to pay any future fees?

Possibly, but it’s much easier to wait until you can confirm she’s in the MLA database and then open the card.

I’m so interested – did she get it reimbursed after being shown in the MLA Database? I’m having a hard time with the same thing. I had a platinum card, then married my husband and now got charged my annual fee. Not being shown eligible under the MLA or SCRA through AMEX. I’ve called and talked to someone probably 5 different times, and just keep reapplying now.

I got denied for SCRA benefits on my Charles Schwab AMEX Platinum (2/3/21):

“The Servicemembers Civil Relief Act provides for a maximum annual interest rate of 6% per year on loans you received before starting active military duty. Our records indicate your account was opened during the active duty time period. Therefore, this account is not eligible for relief under the Servicemembers Civil Relief Act.”

I think this is a mistake. I applied and was approved for the card on Jan 23rd 2021. My active duty started Feb 1st 2021. So I had the card PRIOR to active duty. I am not listed in the MLA database as of today (2/4/21).

My other AMEX Platinum and Gold cards I opened a while ago were approved for SCRA. Very Odd.

I called AMEX and they opened another SCRA inquiry for me. I told them I had the card prior to AD. Still waiting to hear back.

Were you charged the annual fee? If anyone else reads this in the future, just wait until you are in the MLA database before opening your account.

I am a reservist so I am only on for 45 days. I go full time AD next summer when I graduate from med school.

I thought I would qualify for SCRA by starting the new account prior to AD. This worked for me last year.

I have not been charged the AF yet on the Schwab as I just opened the account two weeks ago. My Gold and regular Platinum are waived.

Shouldn’t I still be covered under SCRA for the Schwab platinum? I opened the Schwab account prior to AD. My paperwork and AMEX account corroborate this.

My other AMEX cards were approved for SCRA btw, just not the schwab platinum I opened.

I haven’t been charged the AF fee yet as I just opened the account two weeks ago.

UPDATE: AMEX resubmitted my SCRA request and refunded my annual fees for the cards I had just opened in Jan 2021. It was just a mistake I got denied the first time. AMEX is the best!

Great to hear!

December 2020 updates:

Latest status with Amex on MLA and SCRA. My husband is on active duty and opened the Amex card before he joined the military. I opened the Amex card after he joined the military. He successfully got an approval on SCRA. My SCRA was denied with the rejection reason that my card was opened after he joined the military. Then I had many contacts with different Amex reps to try to get MLA, but all failed with varieties of reasons. For example, MLA can only applies to loan but not the personal credit cards. MLA only applied in the application stage and can’t be added on later. The final answer I got is they have the right to decide if they want to offer MLA or not, even if I’m eligible. Btw, I’m on the MLA database. As there are many other banks offering good credit cards, I’m not going to stick with Amex.

I have been denied MLA benefits as an active duty spouse on a new AMEX platinum card. I am not in the MLA database, but I’m an active duty spouse. All of my friends are (I had them enter their information) who are active duty spouses. Has anyone had success with getting MLA sorted out? No one seems to know what’s going on when I call. I was a dependent under my dad before my husband, so I’m thinking it’s routing back to that somehow but I’m in DEERs with my husband as my sponsor. Very frustrating!!! I opened 4 disputes with AMEX and they denied me SCRA and MLA benefits. Even though I have a delta reserve in my name that has the benefits applied from last year.

Hey Allie. This must be a really frustrating situation. I think this is most likely a DEERS issue, as the MLA database just pulls from DEERS. I would continue engaging with your Personnel Flight or Company until you get to the bottom of why you’re not showing as eligible for MLA. Don’t be afraid to have your husband engage with his supervisor or First Sergeant. Good luck! Amex won’t be able to fix the issue until the MLA database is correctly displaying your MLA status.

12/28/2019

Delta

Active duty

Only me on the Amex card.

$450 charged; 27 days after opening the account was charged.

Spoke with numerous people from Feb-May at American Express. The only request on their site is for SCRA which I was denied for being on Active Duty.

Finally talked to a rep who had me on hold and talked with the “back office” who said MLA was denied upon opening my account but could not provide any additional details.

Are there any data points on getting a prorated AF credit from Amex if activated on orders?

I got the Amex Plat and paid AF in June. In July I started orders. Amex is stating that they do not provide a prorated credit. They will only waive credit if it posted while on orders.

If you opened the card before active duty orders started you should be eligible for retroactive fee waiver under SCRA. I recommend applying for SCRA benefits.

I did apply for SCRA benefits and was approved. The rep said that only if an AF posted while during my active time it would be waived and there is no prorating. I guess I’ll keep trying to call again.

Okay yes, that makes sense, SCRA and MLA only backdates to the time your active duty service starts. If you were charged an annual fee before active duty start date, they won’t refund that. But all future annual fees should not be charged as long as you are on active duty.

1. 5/5/20

2. American Express Platinum

3. I am listed in the SCRA database and not the MLA.

4. No

5. Yes on 5/25/20

Do you know why you aren’t in the MLA database?

I do not. In talking to the DMDC service desk they both receive the same feed from the Navy. I have a trouble ticket in with the service desk.

A quick thought… for those who are applying, are you doing so while logged-in to your Amex so your existing information is pre-filled? That may NOT be the way to go to spark an MLA verification upon application. I would recommend applying while NOT logged in (also in a cache-cleared browser or in private/incognito mode as this may generate a different, potentially more lucrative bonus offer). It’s more work filling out the form, but by doing this you have to re-input your entire SSN as well as you employment status (where you can put “military”). I have no proof this works better than submitting a pre-filled application while logged in, but to me any opportunity to spark a double-check of you MLA status is a good one.

1. 3/2/20

2. Amex Delta Reserve Business

3. Yes, listed on DMDC (and would have been at time of application as well)

4. As far as I can tell, not listed as covered borrower on Account Agreement.

5. Yes, AF charged – posted 20 days after account approval.

I’ve been fighting this AF ever since I paid it – every time I call or chat a rep, they just try to submit another SCRA request. It has been extremely frustrating to be unable to talk to the team that actually handles these requests, or anyone who seems knowledgeable about it. I sent a fax in this week to a number provided by the last rep I spoke to – we’ll see. May need to go CFPB as well, and just emphasize that even if AF fee waiver isn’t required, they have to at least recognize I am covered under MLA – this “we only check at time of application and there’s nothing we can do if we fuck up” BS is getting really old.

I will definitely be following to see if anyone can find a way to resolve this.

Looking through account agreements for my other business / personal cards with Amex, I can’t find a statement that I am a “covered borrower” (under either SCRA or MLA) on any of them. But I am definitely getting waived fees on others cards. Do others have a “covered” statement on their account agreement? If so, is it found on both business and personal cards?

Business cards are not covered under Amex’s new MLA policy. Only personal cards.

Amex will NOT waive annual fees on business credit cards or charge cards opened after 20 Dec 2019. If you have a business card that was opened before December 2019, it appears that the cards are grandfathered in under the old Amex SCRA policy and the fees are still waived.

I do not recommend submitting a CFPB complaint for this. Amex fee waivers on personal cards are already generous and beyond the requirements of MLA. We will eventually kill the golden goose if people keep complaining to Amex about this.

Copy that, won’t push it. I hadn’t been fully up to speed on the demise of MLA waivers for business cards. Was that put out in any official way or has it just been gathered from DPs?

Sorry for any harsh tone. Not intended.

Gathered from data points. Not officially announced in any way.

Hi, I’m a military spouse, I applied for the card two weeks ago and have been refused the MLA on my account, despite mentioning that I was a service member spouse on application and was told to wait until I received the card and apply for the benefits then. They’re now saying they can’t apply the benefit after the application has been made. What’s best to do at this stage, cancel the card or keep fighting for it?

1. Are you identified as a covered borrower in your account agreement?

2. Were you charged the annual fee?

*different Spencer here by the way*

I just filed a report with the Consumer Finance Protection Bureau as I was also told by an employee I would not have to pay the fee/that it would be reimbursed as credit if not waived by the time the fee was due and that did not occur. Maybe there will be strength in numbers, but I will report back if I make any progress through this channel.

Hey Spencer,

I am in the same boat with all of this. Applied for the card in January and got charged the annual fee back when I was a midshipmen. Just recently got approved through SCRA so going forward I will no longer have to pay the fee. As far as getting a refund, I’ve been told that it’s basically not happening which is frustrating because technically I have been active duty since entering the academy back in 2016.

I just wanted to see if there was an update on this issue from anyone. So far I have had zero luck with Amex and getting a refund.

Hey Spencer, thanks for the quick reply. Also I can’t reply to your message directly because its on another chain or something. But in response to your question: I was charged the $550 immediately and they said that I would be reimbursed if I was accepted for the military waiver (SCRA). I found out I was not accepted and applied again (today). Then I found your website and checked to see if I was a “covered borrower” which I was not. I was just on the line with the people from the MLA website and I am not in the system. They think is because I’m a cadet at a service academy even though cadets are still active duty military. This is most likely why I wasn’t automatically referred for the MLA when applying for the card.

Are cadets on Title 10 active duty orders? If you’re not in the MLA database it’s a hard sell (probably impossible) to get Amex to apply MLA benefits to your account.

Cadets are active duty under Title 10 USC 4348. Not sure why I’m not in the database but even I was in there is there any chance Amex would actually give me a credit for the $550?

Amex has not been approving MLA if you are not in the database at time of application. If you are graduating this year or next year, I recommend you keep the card open and apply for SCRA benefits 60 days after you enter active duty. Check the MLA and SCRA database to ensure it shows you as active duty before applying. Hold off on opening new cards until you’re active duty to ensure you get MLA benefits applied.

I am collecting some data below. Ultimately this is up to Amex how they handle MLA cases.

I don’t think you want to poke the bear on this one. Wait until you graduate and are actually on active duty.

“Covered members of the armed forces include members of the Army, Navy, Marine Corps, Air Force, or Coast Guard currently serving on active duty pursuant to title 10, title 14,

or title 32 of the U.S. Code under a call or order that does not specify a period of 30 days or fewer, or such a member Serving on Active Guard and Reserve duty as that term is defined in 10 U.S.C. 101(d)(6).” 32 CFR 232

“(d)Duty Status.—The following definitions relating to duty status apply in this title:

(1)The term “active duty” means full-time duty in the active military service of the United States. Such term includes full-time training duty, annual training duty, and attendance, while in the active military service, at a school designated as a service school by law or by the Secretary of the military department concerned. Such term does not include full-time National Guard duty.” Cornell Law

Alright might as well give that a shot since I probably can’t get my money back from cancelling the card anyway. Thanks for your help I really appreciate it!

if I upgrade my existing card (opened before active duty or SRCA benefit start date) to CC that has an annual fee, during active duty date, would I still get the annual fee waived? as it is not considered as “new credit card”

Probably will not be considered a new account and will not qualify for SCRA or MLA benefits. Better to just open a new account rather than upgrade the card. Plus, opening a new account will make you eligible for the welcome bonus.

I just received the update from Chase. no annual fee / 4% rate will stay for product changes.

“If your account receives interest rate and fee benefit under the Servicemember Civil Relief act or similar state laws (“SCRA”). those benefits will apply for the duration of your SCRA benefit period

Called today to get AMEX PLATNIUM FEE WAIVED, applied for the card 24 Jan 2020, filled out the SCRA info that was denied. I just called the rep and she said because I didn’t request MLA at the time (though I don’t even think AMEX was doing it) it can’t be applied now. I’m going to mail them and if it doesn’t get waived I’ll close the account. Yes, I’m active duty.

Is your account listed as a covered borrower? Was the annual fee actually charged?

I had the same issue, they kept telling me MLA cannot be added to my account after the card was approved, they said the DOD didn’t have my registration when card was applied so the system didn’t automatically enroll me under MLA. They also said there is NOTHING they could do. What the heck!

Hi, here is the reply I received from rep.

To support the men and women who serve in the United States Armed Forces, we are handling your account referenced above in accordance with the Servicemembers Civil Relief Act.

The Servicemembers Civil Relief Act provides for a maximum annual interest rate of 6% per year on loans you received before starting active military duty. Our records indicate your account was opened during the active duty time period. Therefore, this account is not eligible for relief under the Servicemembers Civil Relief Act.

Our records indicate that your Card account is currently receiving relief under the Military Lending Act.

My apply date is 02/08/2020

It is a platinum card

Whether you are listed as active duty int he MLA database here: https://mla.dmdc.osd.mil/

YES

Are you listed as a covered borrower on your account agreement on the Amex card?

YES

Thank you!

Was the annual fee charged?

Hi everyone. I need help. I applied for the Marriott Bonvoy with a $450 annual fee from AMEX around the third week of January. Even though I am deployed overseas, MLA did not automatically kick in and even though I have requested MULTIPLE times the past three months, their answers are always the same.. The most recent customer service rep told me verbatim, “There is nothing that can be done in regards to MLA or SCRA from our end (customer services)”. They already denied my SCRA because I applied for this card while i was on active duty and even though I conintually ask for MLA to be applied since i am on title 10 orders, they responded again, “That process is done at the time of the account approval; however, we have no information about the MLA process or the procedure they follow”.

They also wrote “MLA eligibility is determined automatically at the time of the application ; if it was not added then it means the account is not eligible for that”.

I told AMEX on the phone and customer chat that I have other cards that were covered by SCRA and MLA including my wife’s card but they will not budge and said if i am not satisfied, I can kindly cancel the card!! That got me very annoyed but at this point especially with the travel ban and the headache that i am going through, I think I’ll have to cancel than paying the $450 annual fee. So my two questions are:

1. If I cancel the card, will AMEX claw back the points that I received?

2. Is there anyway for me to somehow get the annual fee back?

Any help on this would be greatly appreciated! I can send some screenshots of the AMEX convo if anyone needs but man this process is annoying..

What is your status in the MLA database: https://mla.dmdc.osd.mil ? Possible solutions are cancel the account and reopen if you’re MLA is showing accurately now. Sorry for the hassle. Are you Guard or Reserves?

I have the exact same problem, I am Active Duty in the database and everything. Got charged an annual fee on my Bonvoy and can’t resolve it with customer service, they keep saying to apply for SCRA again. But, I got it after Active Duty and after 2017. Not a problem on my other Amex cards.

What day were you approved for the card? I think there is a glitch in the Amex system for cards opened near the beginning of 2020.

Are you listed as a covered borrower on your account agreement on the Bonvoy card?

1. Go to your AMEX Account Management page.

2. At the bottom there is a link to “Request Cardmember Agreement”

3. In the agreement you should see the text: “You have been identified as a ‘Covered Borrower’ under Military Lending Act.” on the bottom of page 2.

I would keep insisting to the Amex reps that your account should be handled as a covered borrower. You can also lodge a complaint with the Consumer Financial Protection Bureau or CFPB: https://www.consumerfinance.gov/ or the Federal Trade Commission which is responsible for enforcing the Military Lending Act: https://www.ftccomplaintassistant.gov/

This is very frustrating as it does not appear Amex customer service reps understand their own MLA and SCRA policies. I would keep escalating the case and maybe send an email directly to the CEO of Amex.

I’m sorry this isn’t working on one of your accounts. Please keep us updated if you find a solution.

It was early 2020 and no, I’m not listed as covered borrower on that card agreemnt (I am on others). I got an Aspire a couple months before the Bonvoy (also early 2020) and am also not listed as a covered borrower on that account but, didn’t get an annual fee on that card. I’ll probably call another time or two then consider another avenue. I don’t want to push Amex too hard since their treatment of customers and military has always been so good. But, yes their reps do not know what they are talking about, probably has to do with the way they recently changed the policy. Anytime I try to explain why I should get MLA benefits they ask if they want to submit an inquiry for SCRA, which I know will be denied again, as it should.

Anyway, I have contact info for the person at the CFPB who is responsible for military stuff. She said to reach out to her with stuff like this. So, I may contact her if it is happening to a lot of people.

Update with success, I called and explained my situation. Guy sent a request to check if I was eligible for SCRA or MLA. Apparently there is a way for them to do that internally. 6 Weeks later they said I was eligible for MLA, sent an update cardmember agreement showing me as a covered borrower, and they refunded the annual fee.

I have been trying to resolve this for a whole year, annual fee were charged twice already. They were not familiar with the difference between SCRA and MLA earlier this year so they just kept opening up new cases for SCRA, which of course got denied since I applied the card after joining the military. Last month, a customer service member finally knew what I was talking about and opened up a case for SCRA with a note stating I’m asking to be covered under MLA.

They still denied this by stating that I am not listed in the DOD MLA list, which is not true; I have been active duty for years and I am sure I am listed as active duty in the MLA database. I am really frustrated now not knowing what to do, could someone had this fixed inform me how you did it? Thank you.

Have you actually checked the MLA database? https://mla-ap.dmdc.osd.mil/mla/

I am in the same hole with AMEX in regards to the SCRA and MLA waivers. I appliedin early March 2020 for the card over the phone as an active duty member and inquired about a general waiver. They took my information and said that they would notify me if I was approved. At the time I was not aware of the difference between the MLA and SCRA and was not notified that it mattered that I was already active duty. Now they say it is too late to get the MLA benefits and had me re-apply for the SCRA. Asked to speak with a supervisor who would get back to me in a couple days. Pretty frustrating :/

Was your annual fee charged? Are you a “covered borrower?”

Jason – I am having the same issues and I’m so frustrated! I am not in the MLA database but I absolutely should be. I can’t figure out who to call and AMEX has told me there’s nothing they can do. Everything on the MLA website I’ve tried to call hasn’t been helpful.

My wife created a Delta Amex Reserve card separately and we’ve attempted to contact Amex to waive the fees for her account, but they claim that her account is ineligible for such benefits. Have you had such a situation?

So the fee was charged?

Yes, it has been charged.

Did you add yourself as an authorized user to her account? And to be clear, you are an active duty servicemember?

Apologies for the late reply. I did not add myself to her account as an authorized user. I am the active duty service member and she is the civilian. I already own a Delta Amex Reserve under my own name. She created an entirely separate card account (not authorized user) under the assumption that the annual fee would be waived for her as well.

Add yourself as an authorized user to her account. That will probably trigger an annual fee reimbursement.

So if I apply today for the 25k personal loan will the rate drop to 0% based on MLA or not?

Probably not, the 0% military AMEX loan deal is most likely dead.