Military Money Manual has partnered with CardRatings for our coverage of credit card products and may receive a commission from card issuers. This site may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. Some or all of the cards that appear on this site are from advertisers and may impact how and where card products appear on the site. This site does not include all card companies or all available card offers. Editorial Note: Any opinions, analyses, reviews or recommendations expressed in this article are those of the author's alone, and have not been reviewed, approved or otherwise endorsed by any card issuer. Welcome offers vary and you may not be eligible for an offer. All information about the American Express® Green Card, Marriott Bonvoy Bold® Credit Card, and the Chase Freedom Flex® Credit Card has been collected independently by Military Money Manual. These cards are no longer available through CardRatings.com. The information related to the Chase Sapphire Preferred® Card, Chase Sapphire Reserve®, United℠ Explorer Card, United Quest℠ Card, United Club℠ Card, Southwest Rapid Rewards® Priority Credit Card, Southwest Rapid Rewards® Premier Credit Card, Southwest Rapid Rewards® Plus Credit Card, The World of Hyatt Credit Card, IHG One Rewards Premier Credit Card, Marriott Bonvoy Boundless® Credit Card, and Aeroplan® World Elite Mastercard® Credit Card was collected by Military Money Manual and has not been reviewed or provided by the issuer of this product/card. These cards are also no longer available through CardRatings.com. Thank you for supporting my independent, veteran owned site.

Update: My first $3000 invested with Betterment. And my first $10,000 with Betterment.

I am a do-it-yourself (DIY) investor. I’ve read dozens of books, articles, research papers, and blogs on investing, personal finance, budgeting, asset allocation, and the psychology of investing. I even majored in economics in college. I like making investing decisions and choosing how and where I invest my money.

But, I know that not everyone can or has the desire to devote as much time as I have to researching investing options. That’s why I recommend Betterment to anyone in the military who isn’t a DIY investor like me.

I’ve spent thousands of hours understanding everything I can about investing and money management for military personnel since I started this blog in 2012. I like picking my own asset allocation and investing automatically into low cost, diversified index funds at Vanguard or in my TSP. Then I track my investment performance across all my accounts inside Personal Capital. I don’t try to beat the market: I just try to match its performance.

Even after all that learning I still can’t devote all my time and energy to perfecting my portfolio. My day job as an Air Force officer takes up plenty of time in a normal work week. It can be all consuming when I’m deployed or TDY.

That’s why I have the following investing principles:

- Simple

- Low cost

- Automatic

- Diversified

If an investment doesn’t meet those four criteria, I skip it and move on to the next one. The TSP is a great example of an investment vehicle I like:

- Simple: Only five funds to choose from and Lifecycle Funds available

- Low cost: $0.29 per $1000 invested per year (in 2014)

- Automatic: money is drawn right from your MyPay paycheck, you only need to make the decision to contribute once

- Diversified: The C and S Funds represent all American publicly traded companies. The F and G fund give you corporate and government bond access. The I fund contains 900+ companies in Europe, Australasia, and the Far East.

Betterment also meets all of these principles:

- Simple: easy to set up, easy to automatically fund, easy to see your performance

- Low cost: $2.50 per $1000 invested per year. 0.25% (25 basis points) for their basic digital service, which is what I use and recommend. 3x what Vanguard charges for their cheapest Admiral shares but with so many features for the non-DIY type it makes it well worth it.

- Automatic: Automatic rebalancing of your investments, tax loss harvesting, auto-deposits, portfolios and assets selected to match your investment goals

- Diversified: 13 ETFs make up the Betterment Portfolio. 6 stock ETFs, representing all the major US domestic publicly traded companies and thousands of international companies. 7 bond ETFs which cover government and commercial bonds both domestic and international.

In this post:

Simple Investing with Betterment

With Betterment it’s easy to set up an account. It took me about 45 seconds. The largest US banks are listed and it’s easy to connect your checking account to your Betterment account to get your money moved in. I connected my USAA checking account and moved $500 into a regular taxable investment account to give it a try.

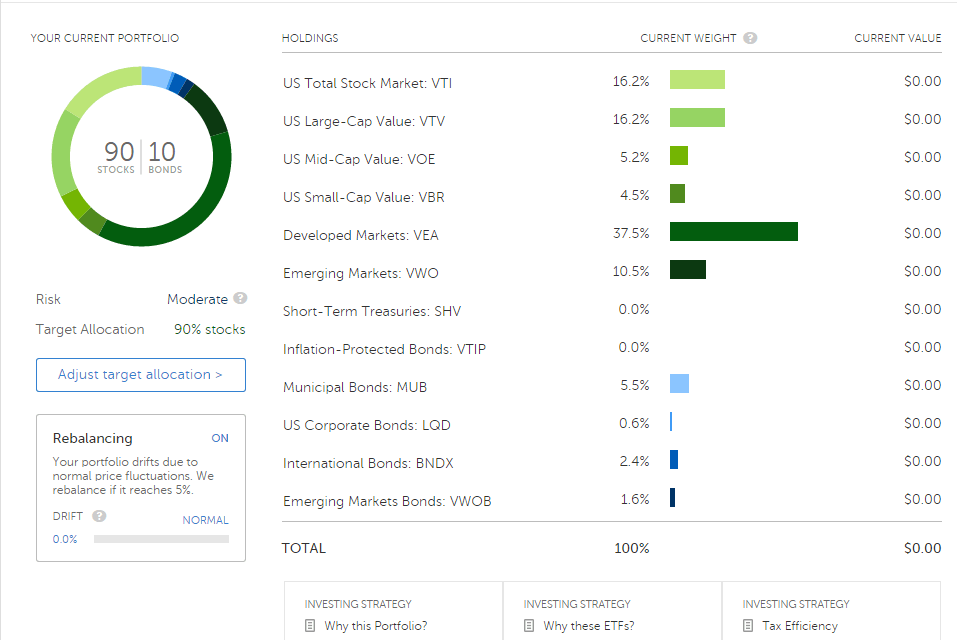

Once you have an account connected, you’ll choose your asset allocation. Again, Betterment keeps it simple with portfolios ranging from no stocks and all bonds to 100% stocks and 0% bonds. As an aggressive investor with a long time horizon (as you should be if your investing for financial independence), I selected a 90% stock, 10% bond portfolio. You can see the asset allocation automatically selected for me below:

Just like that I could now own shares of thousands of US and foreign companies and get a small slice of interest paying debt all over the world.

Low Cost: TSP vs. Vanguard vs. Betterment

When it comes to low costs in investing, there is one undisputed king: the TSP. After that Vanguard has consistently been a leader in providing the least expensive index funds to the average consumer. See the table below:

[table caption=”Expense Ratios of TSP, DIY Vanguard, Vanguard Personal Advisor Services, Betterment” align=”center”]

,Expense Ratio,Annual Cost Per $1000 Invested

TSP,.029%,$0.29

DIY Vanguard,.05%,$0.50

Betterment,.25%,$2.50

Vanguard Personal Advisor Services,.30%,$3.00

[/table]

Betterment offers a comprehensive suite of automatic investing tools for an incredibly low price. At only 0.25% expense ratio, you get features previously reserved for the ultra wealthy at an extremely low price.

Automated Investing with Betterment

With Betterment, you can automate your contributions, rebalancing, and Tax Loss Harvesting. Auto-deposits suck cash out of your checking or savings accounts on a schedule you determine. A pay day 1st and 15th schedule works great for military personnel.

Diversification in the Betterment Portfolio

The Betterment portfolio is built on mostly low cost Vanguard index ETFs. The stock ETFs cover the entire US stock market with a small emphasis on small-cap and value stocks. Based on Nobel-prize winning research by Fama and French into efficient markets, the portfolio also adds developed country international stocks and emerging markets shares to capture growth where ever it can be found all over the world.

The bonds in the Betterment portfolio are selected to manage four categories of risk: “U.S. interest rate risk, U.S. company credit risk, international interest rate risk, and international credit risk.” By mixing corporate, government, and international bonds, risk adjusted performance is increased at all levels.

Cheapest and Easiest Way to Invest if You Are Not DIY Like Me

DIY investing is not for everyone. Even though I’ve done thousands of hours of study into investments it’s still difficult to make the decision of how much money to put into the different funds of the TSP.

How could the average, non-expert be expected to know how to split up their asset allocation in their TSP? That’s why the Lifecycle funds are available. They select an automatic asset allocation based on your years until retirement.

Betterment takes a similar approach, adjusting your risk according to your goals. It takes care of asset allocation, tax loss harvesting, diversification, re-balancing, and all the other little minutiae that can make investing intimidating to newcomers.

If you are not a DIY investor or you don’t have the discipline to stay the course when market conditions become rough, a low cost automated investing service can keep you on track to reach your financial independence goals.

How Military Members Should Maximize Their Investments

- First, maximize your TSP (probably the Roth option) up to $18,000 in 2015 (+$35,000 more into the Traditional TSP if you receive Combat Zone Tax Exclusion pay while deployed)

- Then, open a Betterment Roth IRA for yourself and your spouse ($5500 each, $11,000 total). Spouse does not need earned income if your married filing jointly to fund an IRA.

- Continue to invest additional income into a Betterment taxable investment account

My recommendations: if you are not a confident investor and want a simple, low cost, automatic, and diversified investment account for your Roth IRA and non-retirement investments, Betterment is the best option available after the TSP.

If you are a confident DIY investor, Vanguard is still king of low cost index funds, but the small additional cost of Betterment may be worth it to gain access to their automating diversification and tax loss harvesting.

Don’t you get kickbacks for sponsoring both of those sites? I.E. lower fee percentage rates, etc.

I am an affiliate of Betterment and Personal Capital, meaning I may be compensated if you sign up for one of their services through my links. It costs you nothing but allows me to keep writing on the site. My full advertising policy is here: Advertising Disclosure.

An immense thank you for your advice from a service member’s perspective. I, like you, have done an immense amount of research into investing, but I felt that I could not devote the required time to be successful. I recently started investing a significant amount of our money, that has been sitting in our savings, into Betterment. I looked at others and felt Betterment was the best fit.

I love, love, love the platform and how easy and convenient it was to set-up, deposit, and roll over funds. Being that I am relatively new to the investment game, I was leery about turning my money over to the market because I had very little control over my money, but I knew sitting in my savings was a waste. Your input provided me a little comfort. You are clearly knowledgeable about the market and given your military connection, I feel like I can relate to your experience. Thank you again!

Are you running the risk of violating the wash sale rule by using both TSP and Betterment tax loss harvesting?

Yes, you are at risk of violating the wash sale rule. I discussed this here in another post about Betterment. I do not advise turning on TLH+ if you are making regular contributions to your TSP or other investment accounts.

Right now my wife and I both have Roth IRA’s with USAA and want to start investing in mutual funds for mid-term savings. Since we are both young and aggressively invested would Vanguard or Betterment be better for us?

What are your thoughts on USAA vs Betterment for Roth IRA’s?

In general I am against USAA for investing and prefer Vanguard and Betterment. Vanguard for it’s incredibly low fees and Betterment for it’s ease of investment, inexpensiveness, diversification, automation, and simplicity. The expense ratio on the 2060 Target Retirement Fund at USAA is 1.35%! That is INSANELY high! Betterment only charges 0.25% (+ fund fees, so about .35% approximately) for accounts $10,000-$99,999 and Vanguard charges only 0.16% for their 2060 Target Retirement Fund. If you invested $10,000 with both Betterment and USAA and received a 6% return at both over 50 years, at the end of 50 years your Betterment account would have $385,000 more in it! Fees matter and you can control them, unlike performance. Control your fees and don’t sweat the performance.

What were your thought process for choosing Betterment over Wealthfront? Based on their fee structure, do you think Wealthfront is a better option if your investing less than $100K? However, Wealthfront provides Direct Indexing feature for investment over $100K, which could balance out higher fee compared to Betterment. Thanks and look forward to reading your response. These are the website I read to compare.

https://www.nerdwallet.com/blog/investing/wealthfront-vs-betterment/

https://investorjunkie.com/36355/betterment-vs-wealthfront/

With Wealthfront it is also possible to decrease your fees by referring more people as well.

Great post! Thanks for your insights. I have TSP, Betterment (90 stocks/10 bonds) and Vanguard (Index Trust 500, 100% stocks). I am definitely interested in diversification and am a long-term investor, but I’m seeing that my L2050 TSP fund is outperforming the other two. Do you know if the L2050 cocktail is available at Betterment or Vanguard?

You could create your own L2050 at Vanguard by buying ETFs or mutual funds in the same ratio as the L2050 is https://www.tsp.gov/InvestmentFunds/FundOptions/fundPerformance_L2050.html. However you would have to rebalance monthly, since that’s what the L2050 does. That is a waste of time and too difficult. Don’t try to chase performance. Pick an asset allocation you are comfortable with and stick with it. A Vanguard Target Retirement fund might be what your looking for. It’s similar to the lifecycle funds in that it rebalances often and tilts towards bonds as you approach your target date. Betterment has their own proprietary portfolio that only adjusts the ratio of stocks to bonds, depending on your risk tolerance. The beauty in Betterment is you set it and forget it. No tinkering with the portfolio once it’s set.

Duly noted! Thanks for your response :D

Great Information. Thank you!

I am active dutu AF. Do you think it is wise to start an account with Betterment or keep my TSP?

Until you max out your TSP ($18,000 in 2016), stick with the TSP. The low costs are unbeatable. If you don’t know what asset allocation to select, at least get your money out of the G Fund and into the longest Lifecycle fund available (L2050 right now). This will at least provide some diversification into domestic and international stocks and corporate bonds until you can figure out what asset allocation you like.

Once you max your TSP, look at Betterment for your IRA and taxable investment account.