Military Money Manual has partnered with CardRatings for our coverage of credit card products and may receive a commission from card issuers. This site may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. Some or all of the cards that appear on this site are from advertisers and may impact how and where card products appear on the site. This site does not include all card companies or all available card offers. Editorial Note: Any opinions, analyses, reviews or recommendations expressed in this article are those of the author's alone, and have not been reviewed, approved or otherwise endorsed by any card issuer. Welcome offers vary and you may not be eligible for an offer. All information about the American Express® Green Card, Marriott Bonvoy Bold® Credit Card, and the Chase Freedom Flex® Credit Card has been collected independently by Military Money Manual. These cards are no longer available through CardRatings.com. The information related to the Chase Sapphire Preferred® Card, Chase Sapphire Reserve®, United℠ Explorer Card, United Quest℠ Card, United Club℠ Card, Southwest Rapid Rewards® Priority Credit Card, Southwest Rapid Rewards® Premier Credit Card, Southwest Rapid Rewards® Plus Credit Card, The World of Hyatt Credit Card, IHG One Rewards Premier Credit Card, Marriott Bonvoy Boundless® Credit Card, and Aeroplan® World Elite Mastercard® Credit Card was collected by Military Money Manual and has not been reviewed or provided by the issuer of this product/card. These cards are also no longer available through CardRatings.com. Thank you for supporting my independent, veteran owned site.

After announcing that I would be deployed in 2017 for 6 months, my orders changed. I was not able to execute my 6 month deployment, $50,000 savings challenge. I did not deploy to a combat zone. Instead, I PCS'd to an exciting OCONUS assignment in Abu Dhabi, United Arab Emirates.

My assignment to the UAE came with tax free, Combat Zone Tax Exclusion (CZTE) income for two years, from May 2017 to May 2019 based on my duty location. I plan on saving aggressively with a 50% savings rate, but I do not expect to save $54,000 in six months. I still need to feed the family! We also want to travel and experience the culture as much as possible in this exotic region while we are here.

The CZTE income for the next two years is a fantastic opportunity to sprint towards financial independence. The first priority is contributing 50% of my monthly income to my Roth accounts to lock in the tax free flavor of the money forever.

When you contribute tax free money to a Roth account, the money goes in untaxed, grows untaxed, and comes out untaxed. This is the ultimate tax strategy billionaires wish they could use.

So, I will max out my and my wife's Roth IRA as well as my Roth TSP in 2017-2019.

In 2018, all of my income will be federal income tax exempt. While I'm maxing out my Roth accounts, I can simultaneously convert money in my Traditional IRA to my Roth IRA and potentially reap some tax benefits.

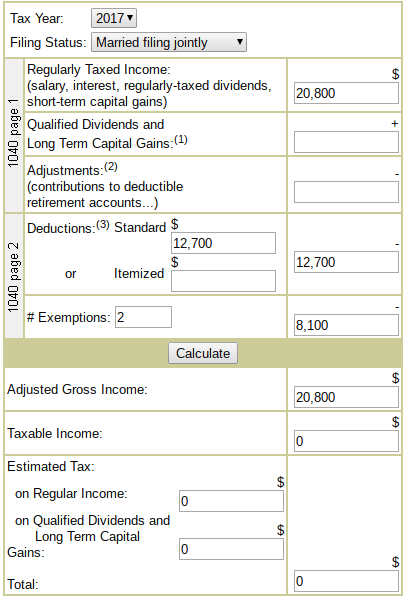

I used the MoneyChimp tax calculator to plan my tax strategy for 2018. See below:

Convert Traditional IRA to Roth IRA While in a Combat Zone

After reading articles on the MadFIentist and Go Curry Cracker!, my strategy for 2018 is:

Converting my Traditional IRA funds to my Roth IRA account up to the married filing jointly standard deduction plus the personal exemptions, which is $20,800 for 2017.

For 2017 the IRS has set the married filing jointly standard deduction at $12,700 and the personal exemption at $4,050 (times two for my wife and I).

That means that you can have up to $20,800 of income (or Roth conversions) and not pay any taxes. Play around with the calculator to understand the concept.

Converting Traditional IRA money to Roth counts as taxable income in the year the money is converted. Traditional IRA money converted to Roth accounts must be taxed in the year converted, since Traditional contributions were not taxed in the year they were originally contributed. Uncle Sam always has to get his cut.

Here is a picture of a Viking statue in Norway to breakup the boring IRA conversion discussion:

However, if your taxable income is extremely low in a specific year (such as a year long deployment), Uncle Sam won't take much or any. Any income up to $20,800 for a married filing jointly couple in 2017 is exempt from federal income tax due to the standard deduction and the personal exemptions.

My plan is to convert $20,800 of my and my wife's Vanguard Traditional IRA contributions to our Vanguard Roth IRA account. This reduces our future tax burden and also give us the option to withdraw $20,800 from our Roth IRA tax free after five years, thanks to the IRS conversion rules. Root of Good goes into the details of climbing the Roth IRA Conversion Ladder.

Since we are converting in a year when we have no other regularly taxed income, converting our Traditional funds into Roth means we never pay taxes on this converted money. It's like contributing tax free CZTE income into a Roth IRA. It goes in untaxed, grows untaxed, and distributes untaxed.

Vanguard Roth IRA Conversion

Vanguard makes the conversion process easy. After logging in, find the search bar at the top of Vanguard's site. Search for “Roth IRA conversion.” Click the article entitled “How to convert a Roth IRA online.” From there, just follow Vanguard's easy to use conversion tool. The website will walk you through where the money it coming from and where it's going.

It should only take a few days to convert and transfer your Traditional IRA funds to your Vanguard Roth IRA. When you file taxes in the following year, you will need to receive tax documents from Vanguard to properly report your conversion and pay any taxes on the conversion. If you have done it right, your tax burden should be low or zero.

Other Ways to Maximize the Financial Benefits of Military Deployment

While you are deployed there are many things you can do to boost your savings, reduce your expenses, increase your investments, and sprint towards financial independence.

- Maximize you and your spouse's Roth IRA contributions (I recommend Vanguard for your Roth IRA) up to $11,000. Deployed CZTE pay goes into a Roth account untaxed, grows untaxed, and comes back to you untaxed. The ultimate tax avoidance strategy.

- Read my book, The Military Money Manual: A Practical Guide to Financial Freedom to learn how to achieve financial independence in the military.

- Contribute $10,000 to the SDP for a guaranteed 10% return (I use some of my emergency fund to top up the SDP).

- Maximize your Roth TSP contributions up to $18,000, then switch to contributing to Traditional TSP up to $54k annually. Same Roth style account benefits as the IRA.

- Convert your Traditional IRA funds to Roth IRA and pay little or no tax on the money.

- Here are 8 ways to save money while deployed.

- And finally why deployment can be the most financially beneficial time in your career.

- You may want to re-characterize a Roth IRA or Traditional IRA contribution if you get a surprise deployment you didn't plan for. Vanguard has instructions on how and why you would want to do that.

Have you tried converting your Traditional IRA to a Roth IRA while deployed and reaped the tax free benefits? I would like to hear if you have made any mistakes or would do anything differently; share your experience!

Another strategy is to harvest long term capital gains. As long as you’re in the bottom tax bracket you pay 0% long term capital gains. Then reinvest at a new basis.

I’m in a similar situation. Do you think it makes sense for me to max my ROTH TSP while deployed for 6 months from Apr-Oct this year with CZTE income, and then put additional tax exempt income into a taxable account rather than the traditional TSP?

Yes, that’s my plan. Max Roth IRA and TSP accounts, then additional contributions for the year into a taxable investment account.

When you say “TSP accounts” do you mean just the $18K Roth TSP limit or are you also including the $36K additional limit available in the Traditional TSP?

Only Roth TSP account. Better to put the additional limit money into a taxable investment account so you only owe capital gains tax on it rather than income tax.

Awesome, thanks for your help!

You previously offered me some insight on reddit for my short tour in the sand. Did you end up taking a CSP assignment instead of the normal deployment? I’m currently in the AOR on a 1 year and if you’re still in the area that you were initially meant to be I vote we still meet at the Fox and talk TSP strategy.

I mainly am trying to decide if it is in fact worth it to go over the $18,000 threshold. I’m looking at swapping my contributions to Traditional to fill out that 18K-54K space but after reading more of the tax code I’m not sure its wise. I know traditional contributions wont be taxed but the growth will be. Why wouldn’t be a better idea to contribute to a taxable account and pay capital gains tax. It seems as though long term capital gain taxes would be lower than that on the Traditional TSP growth if you are receiving a military pension in retirement. You also then have the opportunity to access your money prior to 60 and open up tax loss harvesting options. Would love to hear your thoughts.

Hey Gina, I don’t have easy access to the Fox but if I make it there I will let you know! After studying the problem a bit more, I think it makes sense to do full Roth IRA and Roth TSP contributions up the max for the year with CZTE money. Then all additional contributions to a taxable investment account. Money will go in untaxed, grow untaxed, and only be taxed at capital gains rate when it comes out, until Traditional TSP contributions on which the growth will be taxed as regular income.

Hey Spencer – first off thanks for running the site and congrats with all your success so far.

Question is in regards to contributions prior to deployment. Given what you’ve done and given the tax deductible nature of traditional contributions, if an individual knows they will eventually deploy to a CZTE- wouldn’t it make sense to max out traditional contributions as much as possible, lowering taxable income, and then eventually converting once in the CZTE? This versus maxing out Roth while in a taxable location. Also do you know if we’re able to convert traditional TSP to Roth while still active duty and in a CZTE? Thanks again, cheers.

TJ – thanks for reading and the positive comments. In answer to your question yes, if you know you have a CZTE deployment coming up it would make sense to maximize your Tradtional contributions and then convert them to a Roth account. For instance, let’s say you have year 1 with no CZTE pay and year 2 with all CZTE pay. In year 1, maximize your Traditional contributions to your TSP/Roth. Then in year 2, while your deployed, maximize your contributions to the Roth TSP/IRA AND convert your Traditional IRA funds to your Roth IRA.

However, if you have, say, a six month deployment from July-Dec of a year, since contribution limits are based on the calendar year it makes sense to make all Roth contributions (IRA and TSP) that year, since your taxable income will be so low for the year. It might also make sense to convert your Traditional IRA to Roth IRA even in a year when you have to pay some taxes because the tax rate can be quite low. Play around with the tax calculator linked in the article to see how it works.

Currently there is no way to convert your Traditional TSP to your Roth TSP while in service but there has been discussion by the TSP board in changing that rule. Hopefully they will change that rule soon and allow Traditional TSP to Roth TSP conversions.

Thanks for the reply – just wanted to make sure my thinking wasn’t off there. Here’s to hoping we can convert TSP funds while still AD!