Military Money Manual has partnered with CardRatings for our coverage of credit card products and may receive a commission from card issuers. This site may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. Some or all of the cards that appear on this site are from advertisers and may impact how and where card products appear on the site. This site does not include all card companies or all available card offers. Editorial Note: Any opinions, analyses, reviews or recommendations expressed in this article are those of the author's alone, and have not been reviewed, approved or otherwise endorsed by any card issuer. Welcome offers vary and you may not be eligible for an offer. All information about the American Express® Green Card, Marriott Bonvoy Bold® Credit Card, and the Chase Freedom Flex® Credit Card has been collected independently by Military Money Manual. These cards are no longer available through CardRatings.com. The information related to the Chase Sapphire Preferred® Card, Chase Sapphire Reserve®, United℠ Explorer Card, United Quest℠ Card, United Club℠ Card, Southwest Rapid Rewards® Priority Credit Card, Southwest Rapid Rewards® Premier Credit Card, Southwest Rapid Rewards® Plus Credit Card, The World of Hyatt Credit Card, IHG One Rewards Premier Credit Card, Marriott Bonvoy Boundless® Credit Card, and Aeroplan® World Elite Mastercard® Credit Card was collected by Military Money Manual and has not been reviewed or provided by the issuer of this product/card. These cards are also no longer available through CardRatings.com. Thank you for supporting my independent, veteran owned site.

Enlisting in the military is usually the first real world job of many high school and college graduates. This is your chance to set yourself up for financial independence sooner rather than later.

Your first few paychecks may not be much, but your income will rise quickly. The three most important things to do with your money after you enlist are:

- Save a $1000 emergency fund ASAP

- Buy nothing on credit

- Start your Roth TSP contributions today

You must avoid costly financial mistakes early in your career. By taking these three steps you can avoid the worst mistakes: not saving, getting into debt, and not investing in your financial freedom.

Every year you wait to get your financial life together pushes you that much father from financial independence. Save some money for unexpected expenses, don't get into auto, payday loan, or credit card debt, and start contributing to your retirement now.

If you can do those three things in the first year of enlisting you will be ahead of 95% of your peers and most of your supervisors as well.

Seriously, Save an Emergency Fund

An emergency fund is essential for anyone, but especially young enlisted personnel. It's only a matter of time before finance messes up your paycheck, either by overpaying or underpaying you.

You're in the military. Your job security is about the best in the world. It might take an act of Congress to fire you, but people still get kicked out or voluntarily separate everyday!

Congress frequently uses government shutdowns as a bargaining chip. Your pay gets caught in the crossfire and you're left holding the bag with bills to pay. Don't be caught without some savings set aside.

For many expenses in the military (travel, PCS, TDY/TAD) you are expected to pay for it and then file for reimbursement. This process can take weeks or months!

If you don't have a small emergency fund set aside, these expenses can really hurt and it may be tempting to start using credit card debt.

Setting aside just $1000 is a great way to lower your stress and making sure you can pay all your bills on time. Over time you should grow the fund to cover a few months of expenses, but just setting aside $1000 with your enlistment bonus or first few paychecks will start you off right.

Don't Take Out Loans for Anything!

Buying nothing on credit will keep you from overspending or falling into a credit card debt trap. Spending less than you earn is the first step in achieving financial independence.

If you limit yourself to spending what you have in your checking account, you can't overspend! Set up a checking account at a military friendly, fee free bank like USAA, PenFed, or Navy Federal. Then, only use a debit card for the first few years of your enlistment.

Once you have a higher income and the time to understand how to properly pay off a credit card every month, you can get one, no annual fee credit card.

If you don't have a credit card, you can't get credit card debt. Don't make this mistake. Debit card ONLY for the first few years of enlistment.

Your expenses will be extremely minimal for the first few years of your enlistment. Food, housing, healthcare, uniforms are all provided or paid for you. If you live on base, you can bike to work and buy a beater used car (in cash!) to get off base on the weekend.

There's no reason to put anything on a credit card until your financially mature and responsible enough to only use the card to build credit and reward points. And whatever you do, don't finance a new car at the dealership right off base.

Do You Want to Be Rich One Day?

Starting your Roth TSP contributions now will pay you millions in the future. Changing your rate of return in the compounding interest formula is hard. The easiest thing to do is let your money grow for a longer time.

If you start contributing to your TSP in your teens or twenties, it will have 40+ years to grow before you can touch it. That will yield you thousands of dollars per month in retirement.

Just start with a 10% contribution today. Don't even think about it. Do it before you receive your first paycheck or soon there after and you won't even know it's gone.

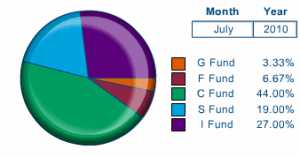

When you have the time, log in to your TSP account and change the contributions away from the G fund to the latest Lifecycle Fund (currently L 2050). That will get your money out of the slow growing (but very safe) G fund into the C fund (S&P 500), S fund (3000+ small cap US stocks), and I fund (hundreds of international stocks).

Later, when you have the time, you can research asset allocations (here's my asset allocation) and portfolios you may want to invest in, but the Lifecycle Funds are a great 90% solution in the meantime.

The reason for the Roth TSP account is simple. Your tax rate is very low as a young enlisted member. Much of your pay is not taxed and by paying the low tax rates now you can lock in tax free income in retirement.

The reason for the TSP vs. a Roth IRA is the low cost of the index funds in the TSP, the automatic contributions from your paycheck, the diversified funds available, and the simple investment options presented.

The TSP makes it extremely difficult to invest unwisely. In the worst case scenario your money grows slowly but nearly risk free in the G fund and you miss out on gains from the stock/bond funds.

The TSP is the cheapest and easiest way for young enlisted personnel to begin becoming investors and owners of companies. Don't think of “investing” and “getting into the stock market” as different from the TSP.

The TSP is the greatest investment vehicle available to all US military personnel. It should be the first thing you try to max out, even before a Roth IRA, especially with the Blended Retirement System in place.

If you're not contributing the full amount to your Roth TSP, don't even worry about opening a Vanguard Roth IRA yet. Max out the Roth TSP (currently $19,000 per year in 2019), then open a Roth IRA account. Skip USAA for investments, as their expense ratios are usually much too high.

If you can do these three things in the first weeks or months of your enlistment, you will set yourself up for an easy, automatic, and successful financial life.

Having just $1000 set aside to cover emergencies, not getting into a cycle of credit card debt, and starting your retirement contributions will not only put you ahead of 95% of your peers and the rest of the US population.

Every year you wait to get your financial house in order is a wasted year. Start when you first enlist and you will have the tools to be financially successful your entire career.

Correct me if I am wrong but I am fairly confident nearly all or almost all of a new military recruits pay is taxed. Unless an E1-3 is getting BAH which I am sure is not the norm, and I would also assume they would not getting BAS either.

This is correct but their tax rate is the lowest it will ever be in their career. With deductions and credits they will probably get all of their withholding returned and effectively pay no or negative taxes. Also, when they do start making tax free income (BAH, BAS, Combat Zone Tax Exclusion pay) they should continue to contribute to their Roth TSP funds to maximize their tax advantages.

Excellent post! I’m a long time reader of Financial Samurai, and stumbled ilupon your recent blog on his website. I wanted to ask you, I’m a physician, and have been growing interest in joining the Medical Reserve, but I’ve read more negatives than positives… So I figured why not get information from someone that’s credible like yourself?

Thanks in advance!

Hi Dex, I’m going to point you to the White Coat Investor. He knows a lot about the military medical career field. I’m not as familiar with it but he should be able to help you out.