Military Money Manual has partnered with CardRatings for our coverage of credit card products and may receive a commission from card issuers. This site may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. Some or all of the cards that appear on this site are from advertisers and may impact how and where card products appear on the site. This site does not include all card companies or all available card offers. Editorial Note: Any opinions, analyses, reviews or recommendations expressed in this article are those of the author's alone, and have not been reviewed, approved or otherwise endorsed by any card issuer. Welcome offers vary and you may not be eligible for an offer. All information about the American Express® Green Card, Marriott Bonvoy Bold® Credit Card, and the Chase Freedom Flex® Credit Card has been collected independently by Military Money Manual. These cards are no longer available through CardRatings.com. The information related to the Chase Sapphire Preferred® Card, Chase Sapphire Reserve®, United℠ Explorer Card, United Quest℠ Card, United Club℠ Card, Southwest Rapid Rewards® Priority Credit Card, Southwest Rapid Rewards® Premier Credit Card, Southwest Rapid Rewards® Plus Credit Card, The World of Hyatt Credit Card, IHG One Rewards Premier Credit Card, Marriott Bonvoy Boundless® Credit Card, and Aeroplan® World Elite Mastercard® Credit Card was collected by Military Money Manual and has not been reviewed or provided by the issuer of this product/card. These cards are also no longer available through CardRatings.com. Thank you for supporting my independent, veteran owned site.

It's been 2 years since I last posted about my asset allocation. I also wrote about my portfolio in 2014. Let's take a look again at how my dollars, my tiny green employees, are working for me.

My investment principles are keeping things simple, low cost, automatic, and diversified. I achieve this by buying and holding index funds offered through the Thrift Savings Plan and Vanguard. I also have a regular Betterment account I opened to understand robo-advisors and compare the cost and performance to a self managed account.

My focus is on what I can control in investing: costs, savings rate, and diversification. My favorite investments are low maintenance investments that don't require any input from me. Dividends get reinvested automatically and I just keep contributing money every paycheck.

I have enough hobbies, activities, and work to occupy my free time. I don't enjoy reading financial statements, picking stocks, or managing and maintaining real estate. I only look at my accounts once a month with Personal Capital when I update my net worth spreadsheet.

Beating the market is extremely hard to achieve even for professional stock pickers, so why bother? I have better things to do with my time. See Jack Bogle's The Little Book of Common Sense Investing for more on this topic.

With those thoughts on my investing philosophy, here's my 2018 asset allocation.

In this post:

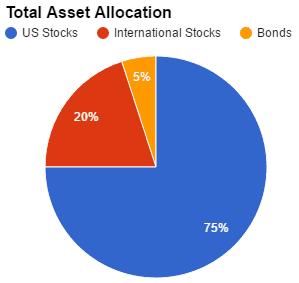

Asset Allocation: 95% stocks, 5% bonds

In 2018 my money is invested the same as in 2016: 95% in stocks and 5% in bonds.

75% US Stocks

20% International Stocks

- Vanguard VTIAX Vanguard Total International Stock Market Index Fund Admiral Shares

5% Bonds

Within this overall asset allocation, I hold 75% of my investments in US stocks through in the Vanguard VTSAX (ETF: VTI) Fund, TSP C Fund (S&P 500 equivalent, the largest 500 companies in America), and S Fund (all other US stocks outside the S&P 500).

Since the C + S Fund = VTSAX, I hold 4x as much C Fund as the S Fund because the C Fund's market capitalization is 4x as large as the S Fund. This is weighting my portfolio by market capitalization.

International stocks make up 20% of my portfolio, all held in the VTIAX (ETF: VXUS) Fund at Vanguard. I've moved away from the TSP I Fund due to it not completely representing the total international stock market. It's a small and probably negligible difference, but VTIAX contains more countries and more companies than the I fund.

My bonds are held 2.5% in government bonds through the G Fund and 2.5% investment grade corporate bonds through the F Fund.

Low Cost and Diversified

Through my index funds, I own a small piece of nearly 10,000 publicly traded companies. I own shares in over 40 countries around the world.

This is a tremendous amount of diversification and helps me sleep easy at night. I never have to worry about a single company or even country going bankrupt. There's no Enron or Bernie Madoff risk in my portfolio.

My average annual fees across all my accounts are 0.06% on average, meaning I only pay $60 per year for every $100,000 I have invested. Check out the fee analysis performed by Personal Capital below.

Automatic Investing

Because I opted into the BRS, I have to spread my TSP contributions over the whole year. The 5% BRS match can be worth thousands every year, but only if you contribute at least 5% of your pay every month, because the match is paid monthly.

If you max out your TSP account before Dec 31 in any year, you could miss out on hundreds or thousands of dollars in matching. I made a few charts on the value of the BRS TSP contribution match so you can see exactly how much extra the government will put into your account.

Also, I calculated the percentage of your pay you should contribute every month so you can max the TSP by the end of the year but still receive the 5% match every month.

For my wife's and my Roth IRA accounts, I am manually contributing and trying to max out the accounts as early in the year as possible. After those accounts are maxed out I will continue investing a percentage of each paycheck into our taxable brokerage accounts at Vanguard or Betterment.

Retirement or Brokerage Accounts

Even though I plan on being financially independent by age 40, I still plan on working after that age. If I could find a well paid job without long hours, I would be happy to work that.

The tax advantages to retirement accounts outweigh the pain of gaining access to the money in the accounts. There are many ways to access money in retirement accounts before age 59 1/2. See Mad Fientist and White Coat Investor for more details.

Especially when you have income from a Combat Zone Tax Exclusion (CZTE) area, you need to stuff your Roth TSP and Roth IRA accounts as much as possible. This pay goes in untaxed, grows untaxed, and distributes untaxed.

You can always access Roth IRA contributions untaxed and penalty free. Do not hesitate to contribute to your Roth IRA if you are in a CZTE area.

I am prioritizing contributing to my retirement accounts and then my regular brokerage account. Based on 2018 values, that will be $18,500 into my Roth TSP, $11,000 in my wife's and my Roth IRA, and the remainder of my savings for the year into my brokerage accounts.

Roth Or Traditional

Most military members have very low taxed income since much of the military paycheck is untaxed. Anything that is an allowance such as BAH, BAS, COLA is not subject to federal income tax.

When you deploy to a CZTE, all of your pay such as base pay and other special pay is not subject to federal income tax. This is the time to prioritize Roth contributions.

Roth or Traditional contributions depend on your family income situation. If your spouse is making a lot of taxable income, you may want to reduce your tax burden today with Traditional accounts. Otherwise, you should probably prioritize Roth contributions.

My taxable pay was so low in 2017 and 2018, thanks to being stationed in a CZTE area, that I converted my Traditional IRAs to Roth IRAs and paid the tax on the conversion. A good strategy for highly paid military members is to contribute to a Traditional IRA if you are not deployed. Then, convert some or all of the account to a Roth IRA when you have a low tax year thanks to CZTE.

Reblancing My Portfolio Annually

Vanguard recommends annual rebalancing or rebalancing if your allocations get more than 5% outside your goal allocation. They have a paper here if you want more info.

I prefer rebalancing annually. I have not yet had to rebalance when the accounts get 5% outside my parameters, since I am contributing monthly and each contribution is essentially a small rebalance.

When I manually contribute to my Roth IRA accounts, I will check to see if my asset allocation is out of whack. If VTIAX grew a bit faster than VTSAX, I will contribute to VTSAX to get back to the allocation I want.

Better* Asset Allocations

Other bloggers have shared their asset allocations:

- Go Curry Cracker 75% US stocks, 18% international, 7% bonds

- My Money Blog 67% stocks, 33% bonds. Stocks: 45% int'l, 45% US, 10% REITS

- The White Coat Investor 40% US stocks, 20% international, 20% bonds, 20% real estate

- Budgets are Sexy 100% US stocks VTSAX

*Are they actually better than mine? No, just different. The problem with selecting an asset allocation is we don't know what sector is going to outperform in the next period.

You can back test the data (with a site like Portfolio Visualizer) all you want, but past performance is no guarantee of future results. I believe it is best to own many asset classes that you expect reasonable returns from rather than betting the farm on one particular sector or idea. Here's a “periodic table” of 8 major asset classes and how they have performed over the last 20 years.

Notice how what's hot for a few years, like Emerging Markets in 2007, drops by over 50% in 2008. And every sector was down in 2008 expect for bonds. Just something to think about when constructing your own asset allocation.

How are you investing in 2018? How much longer do you think the bull market can run? Does the market and economy seem like it's overheating to you?

Disregard my last comments. Looks you did have account ” My Investment Portfolio During COVID-19 | FIRE Asset Allocation”

I had to go to your sitemap to explore and I did find it. But if you go to your tabs up top it take only only to this link.

Thank you I will update the link to my most current asset allocation.

Great break down. I love how you are leveraging the tools in TSP, Vanguard, and Personal Capital to keep costs low and diversify your assets.

I find it interesting you opt out of the I Fund in exchange for VTIAX as well. What do you invest in VTIAX or the ETF version VXUS?

Have you made or considered any changes to you allocations since the pandemic or staying on course?

Also is your permanent portfolio at 45 going to 75% stocks 25% bonds?

Thanks!

I invest in the VTIAX fund. VXUS is the same exact thing, just the ETF version. I don’t know, the old school, old money feel of a “mutual fund” appeals to me. When I picture a millionaire, I picture them owning a mutual fund, not an ETF. Silly, but how my brain works on this one.

I fund is very similar to VTIAX since both are market cap weighted and the largest market caps outside the US are Europe and Japan. Top ten holdings of VTIAX/VXUS are: Alibaba Group Holding Ltd. ADR, Nestle SA, Tencent Holdings Ltd., Roche Holding AG, Taiwan Semiconductor Manufacturing Co. Ltd., Samsung Electronics Co. Ltd., Novartis AG, Toyota Motor Corp., AstraZeneca plc, HSBC Holdings plc.

Top 10 for I Fund are: Nestlé S.A., SAP, Roche Holding Par AG, Total SA, Novartis AG, AstraZeneca PLC, Toyota Motor Corporation, LVMH, HSBC Holdings PLC, BP PLC.

As you can see the VTIAX adds the Chinese stocks like Alibaba and Tencent. I Fund does not invest in Chinese stocks, probably for political reasons for now. While I may not agree with Chinese political leadership, I’m happy to recognize that they have a billion consumers and will one day be the world’s largest economy. Silly to not invest in their largest companies. One of the reasons I hold VTIAX over the I Fund.

Staying the course through the pandemic, see my updated asset allocation here.

Not sure about my permanent portfolio any more. I discussed in my 2014 asset allocation post that at age 45 I would move to a 75% stock 25% bond portfolio. I was six years younger when I wrote that post and now have six more years of study and experience. My perspective has changed a bit and become more nuanced.

I am reconsidering having so much in bonds. With a 40-50 year time horizon, having a more heavily weighted stock portfolio (85% stock, 15% bond or even 90% stock, 10% bonds) might provide better long term returns. After going through the 2020 COVID-19 crash and starting my investing career with the 2008 crash, I think I’ve demonstrated to myself I have the fortitude to ride out the bumps.

One thing I do regret is not having much dry powder (cash sitting around) to throw in when the market crashed. I think I will increase my cash allocation to take advantage of opportunities like the COVID crash. Millionaires on average keep a lot of cash on hand, as revealed by IRS data.

However that being said, there is an argument to be made that once you’ve already won the game, stop playing. What’s the point of having a risky portfolio? The difference between $5 million and $10 million portfolio 20 years from now isn’t business class vs private jet. It might be fly whenever you want vs fly business class whenever you want.

Once you’ve reached a certain lifestyle level, the next lifestyle level is an order of magnitude away. Read “Before the Exit” for a great discussion on Lifestyle Ladders. Essentially once you reach your financial independence number, the upgrade to the next level is so far away as to be meaningless. I’ll write a post about that soon.

Thanks for the awesome reply. Really love your posts and find it extremely helpful and look forward to your post. I think I have already signed up for some of your credit card a while back.

I believe we both started our investment journey at a similar time but I wish I had discovered your blog sooner.

I have been regularly investing in TSP and Roth, but hindsight, I could of done much better had I just spent a little more time understanding the concept, Invest in broadly diversified, low cost, passive index funds which track U.S. and international stock and bond markets rather than letting someone at actively manage it for me and taking the “set it and forget it” approach since early 2008.

After reading Jack Bogle’s book, The Little Book of Common Sense Investing, what stood out for me was his quote, “It’s amazing how difficult it is for a man to understand something if he’s paid a small fortune not to understand it.”

Early in my career I used USAA Managed Portfolio (not at all that great in my opinion) and recently switched to Vanguard Advisory Services (currently charging me 0.30% of all assets under management), mainly because I was not confident and set myself a barrier that I was going to make big mistakes and it would be better for a professional to handle my money. However the more I read, educate myself, read blogs such as your I realize investing is a simple concept that’s broken down very simple 6 principles you had mentioned.

So if you were to have more dry powder what would have been your strategy? Where would that cash go, I’m assuming non-retirement accounts, but curious to hear the asset allocation for that particular scenario.

But as you further stated, that once you’ve already won the game, stop playing concept puts things into perspective…. Look forward to that post as well!

Thanks for signing up for a card. And thanks for reading the more in depth investing posts. The card stuff is fun but the investing posts add more value to society.

I started investing in 2006 when I opened my first Roth IRA at Scottrade with high school summer job money. It wasn’t until paying off all my student loan debt in about 2015 that I started maxing out my retirement accounts.

Actively managed rarely beats passive in the long run. This is the dirty secret of all actively managed funds.

I love that quote from Jack Bogle. Very true.

Vanguard Advisory Service is great if you don’t know the concepts. However, once you learn the concepts (like in my current asset allocation post), it’s cheaper to do it yourself and then you get to capture all the gains.

Agreed that investing is actually incredibly simple. You capture more gains from doing less rather than doing more.

Dry powder – probably a lot in cash, any of the standard high yield savings accounts. Maybe some in CDs, but CD rates aren’t that great at the moment. Yes, this is the tricky part and the reason I didn’t have dry powder – there’s nowhere else to put it other than stocks! When it came time to deploy the dry powder, yes I would put it into my taxable brokerage account. Or solo 401k that I set up for my side business.

Awesome post. What do you say for a military member stationed abroad without an APO address in applying for an investment account? I know most investment companies require a stateside address for opening an account (Vanguard). What do you suggest?

You have no access to any APO/FPO address and you are PCS’d or TDY overseas? Do you have any trusted family member or friend back home where you could use their address? I was able to change my Vanguard addresses to APO but when I opened the accounts initially the address was stateside.

Terrific post. It’s super helpful for a novice investor like myself to see your portfolio breakdown.

I wanted to see if I could get your opinion on something:

I’m an E-7 with 11 years TIS and just now opened up a Roth TSP (very late in the game, I know.) In order to meet the $19,000 annual max, I’m considering withdrawing money out the $127,000 I have in Vanguard’s Admiral VTSAX to offset the contribution deductions from my paycheck. Would this be a savvy move or a foolish one? I’m reluctant to mess with the Vanguard pot of money, which has been performing well thus far, but I also feel compelled to jump on the tax advantages of the Roth TSP.

My primary goal is to maximize retirement savings. I am in the non-BRS legacy retirement plan, and I also have approximately $80,000 in a Vanguard Roth IRA linked to a 2050 target date fund.

Any advice or insight you might be willing to share would be greatly appreciated. Thanks!

First off, congrats on taking the first step by opening up your Roth TSP. It’s never too late to start!

That does not seem like a savvy move. You would be robbing Peter to pay Paul and potentially paying capital gains tax as well. Is your VTSAX in a IRA or brokerage account?

Leave the VTSAX alone and let it grow. Contribute as much as you can to the Roth TSP and grow your contributions until you are maxing it out.

Spencer,

How do you feel about Target Retirement Funds? I have been using the TSP 2050 fund as well as the USAA Target 2050 fund for many years now because I didn’t know any better; from my understanding, the ratios of stock/bond etc for the Target Retirement Funds should be similar to your allocation percentages and then scale more conservative over the years. I am not very happy with my returns on these retirement accounts, however, so should I switch mine to start manually selecting the fund ratios?

Should I rebalance (interfund transfer) the funds already allocated in the 2050 fund to the new ratios?

Also completely off topic question, I would like to use Personal Capital for an overview of my net worth, but am a little concerned with giving all of my bank data to a free service- do you feel concerned at all with your data being compromised?

Thanks!

Hey Dakota. I am a big fan of target date retirement funds, especially when someone doesn’t have the time, interest, or ability to construct their own portfolio. Why are you unhappy with the returns? What ratios would you select if you were to manually build your own portfolio?

What new ratios are you thinking? How did you come up with these new ratios? These are questions for you to consider. Don’t make the assumption that you will outperform the target date funds with a manually built portfolio.

I personally do not use the target date funds because I want a more stock heavy and aggressive portfolio. I don’t mind the big swings up and down because I have a very long investment strategy and I understand the market can be down for years because heading back up.

I am not concerned at all with Personal Capital’s security. They only pull data from your financial institutions, they cannot transact on any of the accounts. The site has been in service for 5+ years and never had a serious security breach. There are many other sites like Mint that also pull in data from all accounts. None of these sites are especially insecure. Read my full Personal Capital review here: https://militarymoneymanual.com/personal-capital/

Spencer,

Thanks for the quick reply. I am mainly unhappy with the USAA 2050 returns and expense ratios when compared to Vanguard’s 2050 returns and expense ratios; not to mention manually selecting funds with Vanguard similar to what you have shown here (VTSAX, VTBSX, etc) would be more diversified and has historically gotten better returns on average.

I would still have the same ratios of stocks/bonds (90/10) that the USAA 2050 or Vanguard 2050 would have, but I would be able to select the funds instead of having them invested automatically.

Thanks for your recommendation on Personal Capital- I may give it a try.

Also thanks for doing these blogs as there is a large number of military folks out there that have this specific situation.

@Dakota – Yes, USAA 2050 fund is .83% expense ratio vs. Vanguard 2055 Retirement Fund (VFFVX) of .15%.

Assuming $10,000 initial investment, $5000 added annually, for 36 years (until 2055) at 6% returns…Total value of USAA fund is $584,102.45, Vanguard is $687,401.34

Over $100,000 difference by switching to Vanguard. I recommend you do it quickly.

Spencer,

You outlined your bonds within TSP, what is your S and C fund breakout percentage each? As someone who is about to contribute to a TSP as a new government civilian (once the CR passes or a real FY budget is had) , I fully agree on your past and current allocation. Oddly enough I have a great and straight forward financial advisor whose done great for me, but he understands that when I move to the civilian role I’m moving half, if not, more of my IRA’s from him to the TSP. Those expense fees CANNOT be touched.

Great post!

-TMV

72% C Fund, 18% S fund. A simple 4:1 ratio to mimic the market capitalization weighting of the US stock market. S&P500 stocks are worth 4x as much as the rest of the US market.

Why do you do VTSAX instead of VTI? Looking to set up my brokerage portfolio now

Mutual funds make more sense to me than ETFs. Expense ratios are the same but I don’t have to mess around with market orders vs limit orders with VTSAX. I just put in my order and it executes after the trading day. Gets back to my personal investing priciples of simplicity, low cost, automating, and diversification.

Simplicity, low/no cost, automated, the diversification and asset allocations you specify, any cash over $10 in the account automatically applied to those holdings below your assigned asset allocation, manual and/or automated rebalancing, income tax considered when rebalancing or selling in a taxable account [would need to tax loss harvest manually], intuitive interface and display, all included in M1 Finance’s no commission, no fee platform. ETFs and individual equities only, but why would you need more.

Probably worth at least checking out.

https://www.whitecoatinvestor.com/how-to-get-your-tax-exempt-tsp-money-in-to-a-roth-ira/

Spencer have you read this? I’d never heard anything about getting taxed on earnings from CZTE Roth TSP but what he’s saying in the last paragraph in the post that sounds concerning. I’d always thought it was like you described but at least so far I can’t find anything on the TSP website that clarifies.

Also, in general for withdrawal from the TSP what are you planning to do? Roll it all into IRAs and withdraw/ladder convert there? Given that they do withdrawals from the entire account combined and don’t let you pick between Roth and Traditional. Seems to be the most feasible assuming you need that nest egg for passive income pre 59.5

Also, for taxable brokerage accounts, which would you recommend for a newer investor that’s just starting to max TSP and IRA? I know you said you started with Betterment as an experiment and also have Vanguard. If you had it to start again would you side with Mad Fientist and say the rebalancing and Tax Loss Harvesting that Betterment offers offsets the higher fees? Or just go Vanguard and do it manually? I’m kind of leaning toward Betterment after reading MF’s post but could easily be swayed haha.

Thanks!

I think White Coat Investor has bad, out of date information in that post. I’m following up with him. Roth contributions from CZTE pay should go in untaxed and contributions and earnings should withdraw untaxed, provided you meet the IRS rules on tax-free Roth withdrawals.

Check out the TSP website: “If you are a member of the uniformed services receiving tax-exempt pay (i.e., pay that is subject to the combat zone tax exclusion), your contributions from that pay will also be tax-exempt. Tax-free earnings if five years have passed since January 1 of the year you made your first Roth contribution, AND you are age 59½ or older, permanently disabled, or deceased.”

For withdrawal from the TSP I am planning on just letting it sit there until I can access penalty free at age 59.5. I’m not planning on fully retiring at age 40, just being financially independent to give myself options. If I did need/want to access the funds earlier, rolling over to a Vanguard IRA and then ladder/convert would probably be the way to go.

For taxable brokerage accounts, after maxing your TSP/IRA it’s a toss up for me between Betterment or Vanguard Target Date fund or manual VTSAX/VTIAX Total US/Total Int’l stock market funds or similar. If you like the additional control of manually picking your asset allocation, go the Vanguard route.

If you can’t be bothered, go Betterment. My brother is an accountant but has no time/energy for investing. He loves the simplicity of Betterment. I recommend Betterment to all of my siblings and cousins who want to invest but don’t want to make it complicated or don’t have enough funds to open a Vanguard account. Personally, I am happy with Vanguard’s low fees and will continue to allocate most of my taxable investments there.