Military Money Manual has partnered with CardRatings for our coverage of credit card products and may receive a commission from card issuers. This site may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. Some or all of the cards that appear on this site are from advertisers and may impact how and where card products appear on the site. This site does not include all card companies or all available card offers. Editorial Note: Any opinions, analyses, reviews or recommendations expressed in this article are those of the author’s alone, and have not been reviewed, approved or otherwise endorsed by any card issuer. Welcome offers vary and you may not be eligible for an offer. All information about the American Express Green Card, Marriott Bonvoy Bold Credit Card, and the Chase Freedom Flex has been collected independently by Military Money Manual. These cards are no longer available through CardRatings.com. Thank you for supporting my independent, veteran owned site.

Hello, my name is Spencer. I'm a twenty-something officer in the US Air Force and the sole writer of this site, Military Money Manual. I love writing and reading about personal finance and planning our future with my wife. You can find out more about me and this site here.

This page is quite long. It covers almost all of my overall plan to achieving financial independence by age 40 while serving on active duty military status, starting with over $100,000 in student loans when I commissioned at age 22. It should get you started navigating this site and discovering everything I've learned about early retirement, financial independence, money management, and personal finance in the military.

Let me start by saying I like my job. I've served in the Air Force since 2010 and I can honestly say most morning I love driving into work. I work with some of the smartest, loyal, and all around best people in the world.

However, I know that this job isn't forever. In an era of defense drawdowns, sequestration, spending cuts, and the end of the wars in Afghanistan and Iraq, military jobs are going to be harder to hold on to.

One day my service contract will expire. When that day comes, I want to be in a position to decide what to do with my life. If I'm loving my Air Force job, then I'll stick with it. If I'm not, I want to have the financial independence that I can say “see ya!” and get out to do something else. Or nothing else, if I want.

In this post:

What is financial independence (FI)?

This chart, from the book Your Money or Your Life defines it best for me:

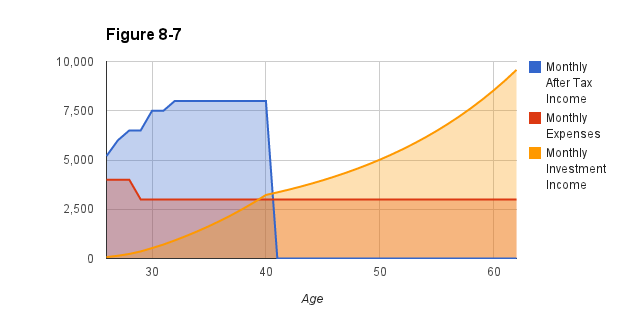

At the age of 40, I want my monthly investment income to equal my monthly expenses.

To generate enough annual passive income for the rest of our lives, we'll need to have saved and invested 25-33 times our annual expenditures. (This is based on a safe withdrawal rate of 3-4%). So if we expected to spend $36,000/year, we would need $1.2 million of invested assets.

Another way to think of it is for every $25-33 you have invested, you are allowed to spent $1 a year.

How will we get to 25-33x in 15 years while serving on active duty? Read on to find out…

Where it All Began

I've always been interested in investing, saving, and managing my money effectively. I opened my Roth IRA account when I was in high school and bought my first stock at the age of 16. I worked jobs every summer from age 16 until I graduated from college.

After I graduated college, my parents introduced me to Dave Ramsey. I never really liked his style or his ability to repackage common sense and sell it at an incredible markup. Or his use of churches to further his financial gain. But enough on Dave…

I started reading Get Rich Slowly and other personal finance blogs soon after. After I graduated from my initial training course for the Air Force, I checked out every book on personal finance and money management I could find from the base library. I was a bit obsessed.

After internalizing all of the collective wisdom of the PF blogosphere and every book I could get my hands on, I came up with a plan of action. At first, I merely wanted to pay off all my student loans, save for retirement, and have some beer in the fridge. But then I started diving into the minutia of early retirement and financial independence. After crunching the numbers, I decided I had a new goal. Financial independence by age 40, 4 years before I'm eligible for my military pension.

My Financial Situation After Graduating College

I graduated college in May 2010 with:

- $1000 in my checking account

- $8000 Emergency Fund

- $6000 in a Roth IRA

- $1700 Ford Explorer

- -$60,000 in student loans

For a net worth of: -$43,300 (Now I track my net worth with Personal Capital)

Housing was provided for, as were utilities, because I lived on base. My parents gifted me a 10 year old Ford Explorer for a college graduation present, which was gratefully accepted. My student loans were in a grace period for 3 months after graduation.

Base pay for an O-1 (2nd Lieutenant) with less than 2 years of service at the time was $2745/month, before taxes. After taxes, additional pays and incentives, and SGLI (government subsidized, cheap military life insurance), I had about $1200 in my pay check. My first few months of post-college budgeting looked something like this (per paycheck):

- $1200 income

- -$120 Roth IRA (10% of my after tax income)

- -$125 Sallie Mae student loans (2.5% APR)

- -$250 USAA Commissioning Loan (2.99% APR)

- -$150 savings for car maintenance and insurance

- -$80 for my cellphone and internet

- -$200 into saving account for random fun things

- -$150 leftover for groceries, gas, going out, beer, entertainment, miscellaneous

I was budgeting down to the dollar. It was tight. Sometimes, I use a credit card to spend money I didn’t have in my checking account. I could always cover it with the next paycheck, but I was setting a dangerous precedent, and I knew it.

I also knew that if I could hang on for just a few years though, I’d start making a bit more money. Total compensation for military servicemembers rises rapidly in the first few years of their service. A US military officer in any branch, with no special pays, will see their biweekly paychecks rise from $1200 as a brand new officer to $3000 in 4 years as a captain. That’s going from $36,000/year to nearly $80,000/year (before taxes) in just 4 years!

I knew that I needed to get my crazy amount of student loan debt under control. At graduation it represented 200% of my annual after tax pay. Just the minimum payments on these loans consumed 35% of my paycheck! I made student loan debt repayment my first priority.

I also knew that time is on the side of the young investor. I had opened my Roth IRA in high school and knew that regular contributions, invested wisely, would eventually grow into a large retirement nest egg. Retirement savings became my second priority.

Finally, from hearing horror stories around the web and from family and friends, I knew car ownership could become ridiculously expensive. I set aside $150 of each paycheck to cover maintenance and insurance costs. This was my third priority.

Now that I had my priorities, I spent the remainder of my money on fun things. I didn’t have much a goal, other than to achieve my three priorities and have some fun doing it.

My Financial Plan After College Graduation

Here was the plan I followed in college and immediately after graduating:

1. I only hold checking and savings accounts at banks that don't charge fees. My go-to bank in 2010 was ING Direct (now Capital One 360) and USAA. Today, I do all my checking and savings account banking with USAA. For online spending, I primarily use whatever credit card is offering the best cash back. For in person spending, I use a debit card, to keep impulse buying in check.

2. I never allowed myself to spend more than I had, in high school, college, and beyond, so I've never paid the credit card companies a dime in interest. This is probably one of the smartest things anyone can ever do. Once you fall into the trap of easy credit, it is so difficult to dig out. Most of the success stories you read about online begin with people drowning in credit card debt and eventually paying off their burdens.

3. Educated myself by reading books from the library, blogs, and other online resources. This is probably the most important step towards financial independence/retiring early (FIRE).

4. Minimized my student loan interest rate with a USAA Commissioning Loan (dropped from 6.8% to 2.99%). The USAA Commissioning Loan is an excellent way to drop the interest rates on any current debt you have. It’s also a great way to begin a lifetime of slavery debt. Use it carefully.

5. Built a $10,000 emergency fund. This was primarily accomplished by investing the USAA Commissioning Loan into USAA CDs that were offering 4-5% interest. This covers 4 months of our expenses. It’s also a nice, round, 5 digit number that reassures me that I can ride out most financial difficulties.

6. Aggressively began paying off my debt as soon as I graduated college, making payments of $1000/month with $696 minimum payments. This set me up to pay off my student loans 5 years ahead of schedule and save thousands of dollars in interest payments.

7. Maximize my Roth IRA contributions by automatically allocating money each month to my Roth IRA account in MyPay. Because of this aggressive saving, we saved enough to put a down payment on a condo in 3 years.

8. Build my savings for future expenses, such as a wedding ring, car, or house down payment. I recognized that in the near future I would probably have more expenses, both recurring and one-time.

My Priorities as of December 2013

Some things have changed since I graduated college.

- We got married

- I got promoted (twice)

- I got deployed (twice)

- We bought a house

- We moved three times

- We saved a $10,000 emergency fund

- I learned much about financial independence and early retirement

Because of all these changes, my priorities have changed a bit. Especially important has been continuing my financial education with big picture thinkers like Mr. Money Mustache, Early Retirement Extreme, and Doug Nordman's Military Guide.

The global financial big picture has also changed dramatically. New financial products have become available that were not available 3 years ago. The Roth TSP option became available.

We're Not Signing Up for the “Great American Plan”

Because of all these changes, we started thinking a lot about “the great American plan.” This plan is especially prevalent in the military, which tends to be an overly conservative institution.

You know this plan well:

- Graduate high school

- Go to college

- Take on massive student loans

- Graduate college

- Get a low paying job you hate (or no job, these days)

- Buy a car you can't really afford, take on more debt for it

- Find a wife/husband

- Get married, spend $25,000 on a wedding

- Have a baby

- Buy a house you can't afford, watch its value fall when the housing market collapses

- Continue working in jobs you hate to pay for things you don't need to take your 2 weeks of vacation per year (4 weeks if you're military!)

- Retire at 60-65 (or don't, because you haven't saved enough)

My wife has never been one for the plan. I was onboard until I started reading more and questioning a lot of assumptions:

- What if I actually like my job and it pays a pretty competitive salary?

- What if I pay all my student loans off in 5 years instead of 10?

- What if instead of making a $200 per month car payment, I instead spend that on travelling around the world?

- What if we get married, but only spend 25% of the average American wedding cost?

- What if we never want to live in the same place for more than a few years and we can rent cheaper than buying?

- Will we really need to retire on 80% of my annual income?

- What if there was another way to play the game?

What I found was that there IS another path. A path towards financial independence and the freedom to retire early, start a business, take on a second career, spend time travelling, learn a new language, or do whatever you want.

So as of today, December 2013, this is our current roadmap to financial success and lifelong happiness:

Our 5 Step Plan for Financial Independence

- Pay off Debt – I have just under $30,000 in student loans to go. We continue to not accumulate any new debt by automating our savings, spending wisely, and never buying anything we can't pay for immediately. I recently retired my USAA Career Starter Loan, which can be an awesome opportunity to start your military career by paying off your existing higher interest debt or can be a ball and chain you wear for 5 years.

- Max the Roth IRA – since we're married, we can contribute $11,000 per year into our Roth IRA fund. Since Roth investment options allow you to be taxed now rather than when you withdraw the money, and our effective tax rate is under 10% with much of our income tax free (Combat Zone Tax Exclusion, BAH, BAS, etc), we are choosing to pay our taxes now. Since Roth IRA contributions can be withdrawn at any time, we are happy to contribute the max every year and invest in diversified Vanguard funds.

- Invest the maximum amount in the Roth TSP – Ever since the Roth Thrift Savings Plan option became available, we have worked to invest the maximum allowable amount ($17,500 in 2014). The low cost index funds in this retirement account, combined with our very low tax rate, make this our second investment option (after Roth IRAs). Because my pay is essentially untaxed (through tax free combat pay), the money goes in untaxed, grows untaxed, and can be withdrawn after age 59.5 untaxed. Amazing!

- Enjoy life now – we love saving for the future. We also love living in the moment. Balancing the two is a constant struggle for many people. We have chosen to spend money on the things that maximize our happiness: family, travel, friends, and good food. We can afford these things and still save for FI because of our lifestyle choices. We have no car payment so we can put away $200 per month for travelling. Small things like this make a world of difference.

- Invest in our “Gap Fund” – we are planning on becoming financially independent and “retiring” early in our lives at the age of 40. That leaves 20 years from when we become financially independent until we can access our tax advantaged retirement accounts without penalty, at age 60. In those 20 years we’ll rely on our “gap fund,” a collection of taxable investment accounts and perhaps a property or two providing us with dividend payments, capital growth, rental income, and interest payments. Since we take a long term investing view, we invest with low cost, diversified Vanguard funds.

As of May 2013, we are well on our way to achieving FI by age 40. We are rapidly retiring my remaining student loan debt. Now that my USAA loan is paid off, our monthly minimum student loan payment has dropped to $225 from $696. Because the interest rate on this debt is so low (1.75% and 2.75% for the two remaining Sallie Mae loans), we are beginning to make contributions to our gap fund.

Our income continues to increase through time in service pay raises and promotions in addition to another income generating projects such as AirBnB and this website. My wife’s start up company is beginning to take off and may be producing income within a year or two.

We are very excited for what the future holds and to watch our progress towards financial independence at age 40. Along the way to our goal, I'll share tips and tricks on how I grow my wealth while serving in the US Armed Forces. Check back on this blog for updates!

Thanks for all the work you’ve put into this site, Spencer. I’ve periodically checked back over the last few years and its always helpful and reassuring. I now even point some of my troops to it (the ones willing to listen and do some math for themselves at least).

I am currently an E-5 in my mid 30’s contributing almost the max to my Roth TSP. This sets me up to retire comfortably when I can finally withdraw from it at 59.5 but leaves money a little tight for the here and now. Without tightening my belt even further, how would you start building the “Gap Fund” you talk about?

Would you do something like decrease your TSP contributions in favor of regular investments, or would you contribute the max to an IRA for the freedom to withdraw the contributions to be used as the Gap Fund? Or maybe there is a third option I am not seeing? I am trying not to assume any promotions but do plan on serving for at least 20 years total.

Nick, I appreciate you reaching out. The site has been fun and rewarding to work on since 2012. It’s fun to have long time readers and companions on the journey to FI.

Thanks for sharing the word with your troops. If I can help one young officer or enlisted guy or gal get their finances right, then it’s all been worth it.

Let’s break down the gap fund. Let’s assume a servicemember enlists at age 20 and wants to financially independent at age 40. You’ll need to fund 20 years from age 40 to 59.5 until you can touch your retirement funds without penalty.

Let’s assume FI annual spending is $60,000 or $5,000/mo. If you retire an E-7 with 20 years you’ll have about $27,000 of pension the first year (inflation adjusted every year after). So now you need to make up $33,000 of income per year.

There are a few options you could do. Fund a Roth IRA for 20 years * $6000 = $120,000. That’s 4 years so now you can get to age 44 and only need to cover 16 years until you can tap your retirement accounts without penalty.

$33,000 * 16 years is $528,000. Withdrawing $33,000 per year from $528,000 is a 6.25% withdrawal rate. A little high if you wanted to be guaranteed to last 30+ years, but you only need it to last 16 years until you can access your retirement accounts. You can play with the numbers here on Engaging Data: https://engaging-data.com/will-money-last-retire-early/ but you can see how with a little creativity you can make this work.

You may want to investigate a Roth conversion ladder: https://www.madfientist.com/how-to-access-retirement-funds-early/