Military Money Manual has partnered with CardRatings for our coverage of credit card products and may receive a commission from card issuers. This site may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. Some or all of the cards that appear on this site are from advertisers and may impact how and where card products appear on the site. This site does not include all card companies or all available card offers. Editorial Note: Any opinions, analyses, reviews or recommendations expressed in this article are those of the author's alone, and have not been reviewed, approved or otherwise endorsed by any card issuer. Welcome offers vary and you may not be eligible for an offer. All information about the American Express® Green Card, Marriott Bonvoy Bold® Credit Card, and the Chase Freedom Flex® Credit Card has been collected independently by Military Money Manual. These cards are no longer available through CardRatings.com. The information related to the Chase Sapphire Preferred® Card, Chase Sapphire Reserve®, United℠ Explorer Card, United Quest℠ Card, United Club℠ Card, Southwest Rapid Rewards® Priority Credit Card, Southwest Rapid Rewards® Premier Credit Card, Southwest Rapid Rewards® Plus Credit Card, The World of Hyatt Credit Card, IHG One Rewards Premier Credit Card, Marriott Bonvoy Boundless® Credit Card, and Aeroplan® World Elite Mastercard® Credit Card was collected by Military Money Manual and has not been reviewed or provided by the issuer of this product/card. These cards are also no longer available through CardRatings.com. Thank you for supporting my independent, veteran owned site.

What percentage of your monthly pay do you need to contribute to your military Thrift Savings Plan with Blended Retirement System (BRS) to max out in December 2026?

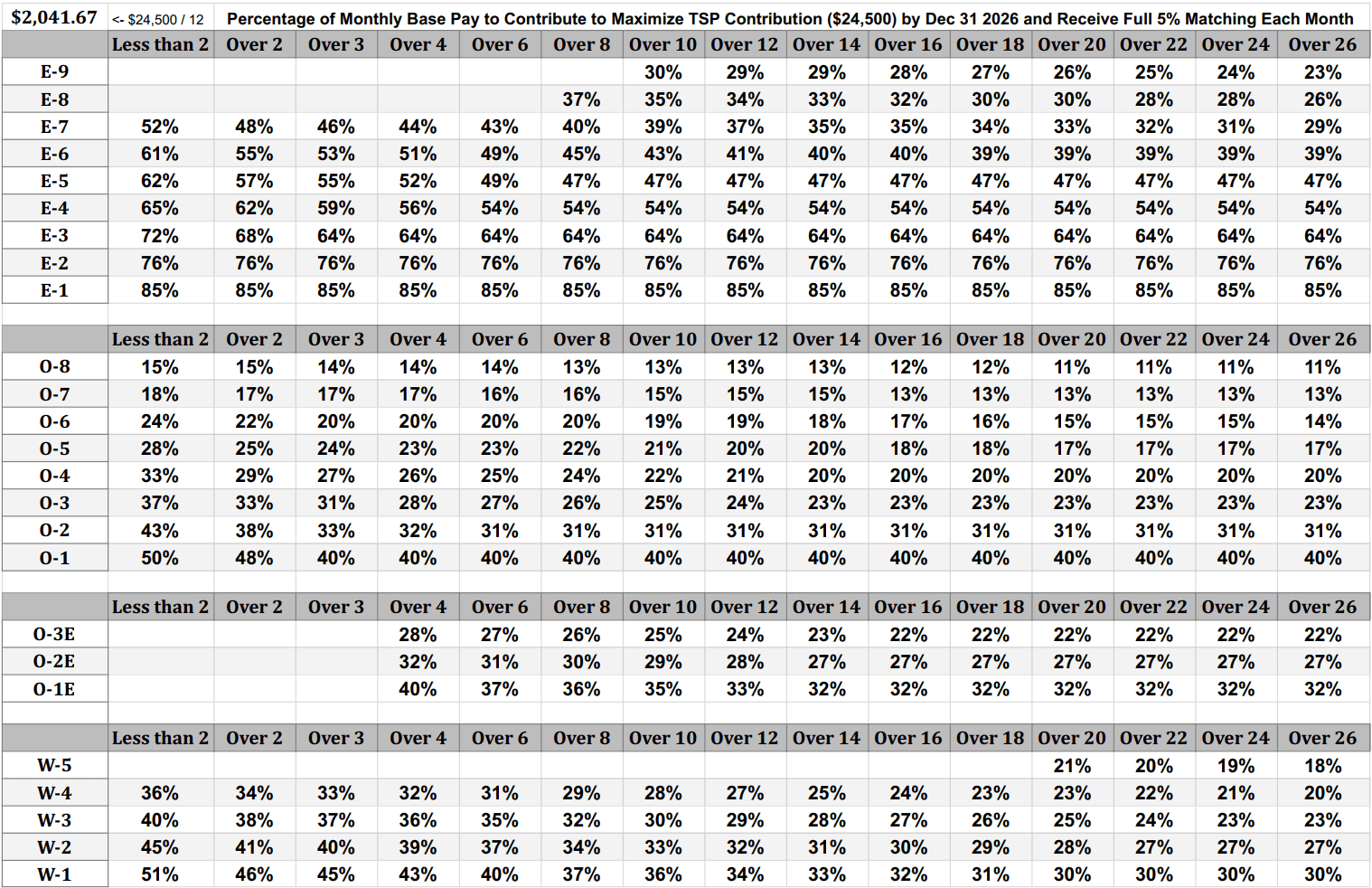

2026 TSP Percentage Tool

Target the $24,500 Limit Without Missing the BRS Match

Here are the 2026 military TSP BRS matching contribution maximizing tables, based on the 2026 military pay charts and TSP contribution limit moving up to $24,500.

In order to receive your full 5% military TSP match, you must contribute at least 5% a month to the TSP and NOT max it out too early before December of the year. The match is paid monthly. You must make at least a 5% contribution in every month to receive the full 5% match.

The easiest way to do this is to spread your TSP contributions evenly over the 12 months of the year.

Available as a PDF download or Excel Spreadsheet or click the images for full screen image.

The military TSP matching through the Blended Retirement System (BRS) is an excellent way for military servicemembers to build their retirement savings.

If you want to learn more about successfully investing in your TSP, check out the Confident TSP Investing Course.

I cover investing in the Thrift Savings Plan in my Military Money Manual podcast, available on Spotify and Apple Podcast or embedded below.

We also covered the TSP for absolute beginners and what your first two years in the TSP looks like in episode 100 of the podcast:

The BRS allows you to earn government matching up to 5% of your pay, so your military Thrift Saving Plan (TSP) account can grow faster. This is a improvement to the military retirement system for the more than 80% of servicemembers who will not earn a 20+ year military pension.

Thanks to BRS matching contributions, I added an additional $4,600 extra into my Traditional TSP from 1 Jan – 31 Dec 2021. Compounded over 40 years at 7%, that matching contribution grows to $68,000.

Individual Retirement Accounts (IRAs, both Roth and Traditional), are $7,000 for 2024. $583.33 per month to max out your Roth or Traditional IRA.

Optimize your TSP Match Contributions With BRS

The BRS TSP match can be worth thousands per year if optimized correctly. The limiting factor is you have to contribute 5% each month, as the match is paid monthly.

Therefore, you do not want to make all of your $23,500 of contributions (the annual elective deferral limit) in the first 6 months of the year: you must space out your contribution for the full year if you want to receive the full match.

I used to front load my TSP contributions as fast as possible at the beginning of the year. Under the BRS, this is no longer optimal so I changed my contribution strategy.

Don't worry about going over the annual $23,500 limit. As long as you don't have another employer retirement account (401k, 403b, solo 401K), the DFAS computers will limit your final contribution to ensure that you max out the account without going a penny over. There was a glitch in 2021 and 2022 that allowed over contribution or “TSP spillover” but this has been fixed.

How Much Should I Contribute to the TSP to Get the Full Match?

The tables above shows the percentage you should contribute monthly for all enlisted, warrant, and officer ranks up to O-8 and 26 years of service. If you are an O-9 or have over 28 years of service, please have your aide run the numbers for you.

If you want to maximize your TSP contribution for the year 2022 ($22,500) and receive the full 5% TSP match you are eligible for, you must contribute at least 5% to the TSP every month.

The formula is pretty simple. Take your maximum elective deferral contribution limit of $23,000 in 2022. Divide by 12 months = $1,958.33. Now divide $1,958.33 by your monthly base pay to get a percentage of contribution.

For example, if your base pay is $5,000/month, $1,958.33 / $5,000 = .391 or 39.1%. Round up to 40% because you can only elect contributions in whole percentages.

If you contribute 40% of your $5,000 base pay, you will deposit $2,000 each month into the TSP, Roth or Traditional.

The match always goes into the Traditional TSP for tax reasons. You will still get the match if you contribute to your Roth TSP, but the match will go into the Traditional TSP. You cannot change this. The match does not count against the $23,500 limit. It counts against the “annual additions limit” which is $72,000 for 2026.

Side note

So by November 2026, you will have contributed $22,000 to your TSP. Your match will be worth $5,000 * .05 = $250 per month or $3,000 for the entire year.

In December 2024, because you only have $1,500 left of contributions ($23,500 – $22,000), the TSP or DFAS computers should only allow you to contribute $1,500 and the remaining $500 will be in your December or January paycheck. A nice Christmas or end of year bonus!

Now you have maximized your annual contribution and received the full 5% match every month of the year.

You can change your contribution election on myPay for Navy, Air Force, and Army.

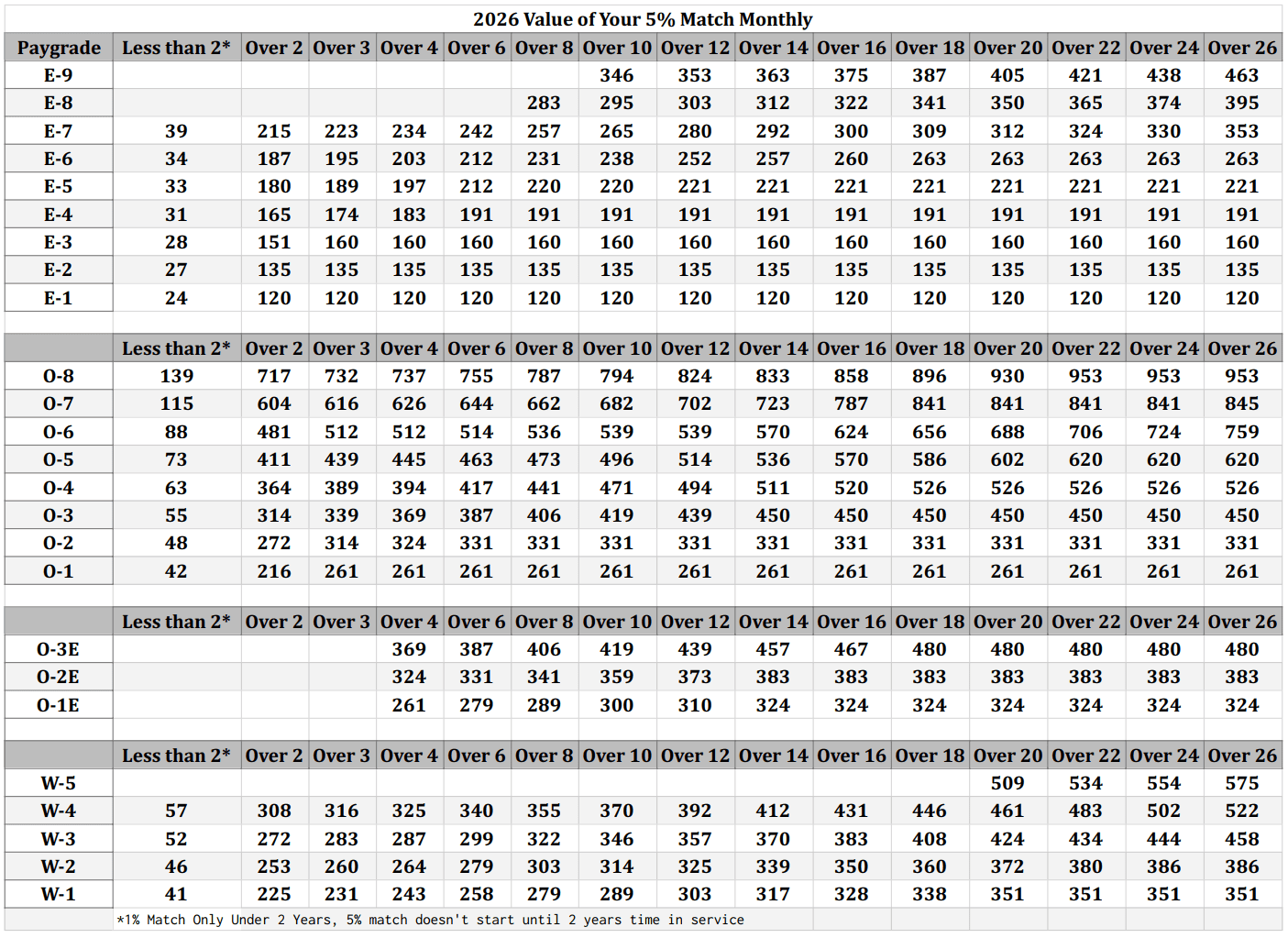

How much is the military TSP match worth monthly 2026?

If you contribute at least 5% of your pay to the TSP under BRS, you may wonder how much that is worth each month.

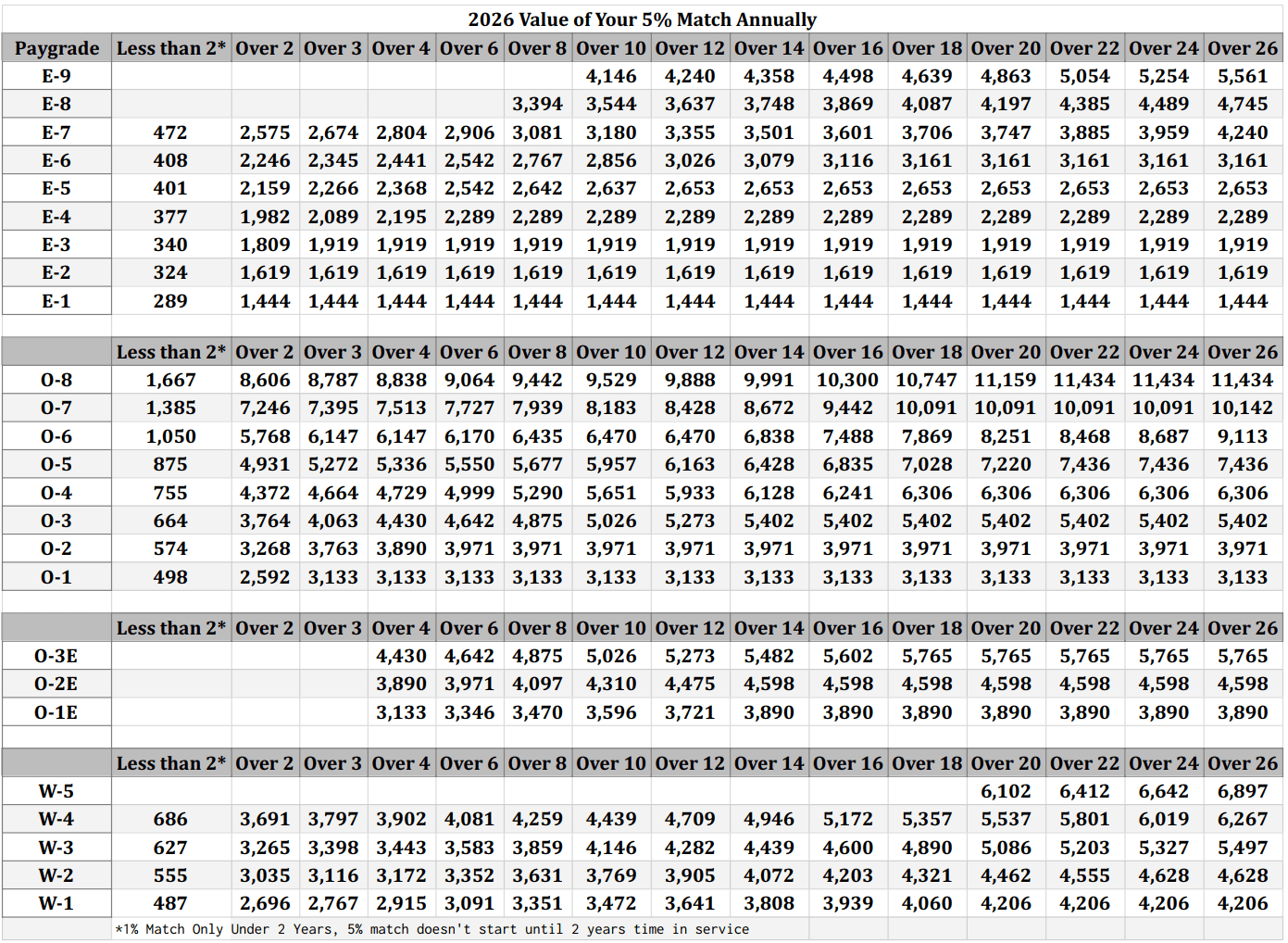

How much is the BRS TSP match worth annually?

If you receive the full BRS match every month this year, it can be worth thousands of dollars depending on your pay grade and time in service. Compounded over a few years or decades, your TSP match can grow to tens of thousands of dollars by retirement age.

This additional investment can provide you with substantial additional income after financial independence or retirement.

Available as a PDF download or Excel Spreadsheet or click the images for full screen image.

Here is the 2026 military pay chart I based all my calculations off of.

Military TSP Match FAQ

The military automatically matches 1% of your basic pay into your military Thrift Savings Plan account. If you contribute at least 5% of your military pay to either the Roth or Traditional TSP, the military will contribute another 5% into your Traditional TSP. This can be worth $1,000s every year.

Yes! Roth TSP is matched. The match, however, will go into your Traditional TSP account. When you open a TSP, you have 2 accounts inside the TSP: A Traditional account and a Roth account. You can contribute to either one and receive up a 5% match from your employer monthly. However, whether you contribute to Trad or Roth, the match ALWAYS goes into the Traditional account.

At a minimum you should put in 5% into your TSP. If you are enlisted or below the rank of O-4 (major, lieutenant commander), you should probably contribute the 5% to your Roth TSP. As your income grows, you should eventually contribute the maximum $23,500 per year to your military TSP account, while still ensuring you get the 5% match every year.

You can if the tax form or software asks you to report it. However you have already paid tax on this money before it goes into your Roth. Therefore, it does not lower your taxable income in that year and does not usually need to be reported.

To maximize your military TSP match you must contribute at least 5% of your pay every month from January to December. Therefore you do not want to max out your contribution earlier in the year. There is a chart on my site that will show you what percentage to contribute.

No, the standard TSP limit does not include matching. In 2025 you can contribute the full $23,500 and get matching on top of that, up to the “annual addition limit” of $70,000. The standard TSP limit is called the “elective deferral limit.”

If you want to max out your TSP contribution per pay period, you need to do some math. Take the total annual contribution limit $23,500 and divide by the number of pay periods (12). That's $1,958.33 per month. Divide that by your base pay to get your monthly minimum contribution to max out your TSP by December 31.

thank you for the updated charts

I would like to thank you for your site and information. I am actually doing this for my wife who is a physician and the VA actually recommended your website for us to figure this out…we really cannot find any help around here and have gotten the run around.

Currently she has a 5% match but is contributing so little that at times I am not sure if it is helping. This is her 10th year as a VA physician (she is part time) and her monthly pay is $5600 (gross) with two payments a month. I am not sure which column to follow on your excel sheet (if any).

If her pay is $2800 gross, she gets $28 for TSP Basic and $112 for TSP matching…my goal is to put more away and reduce our taxes. Any suggestions what this number would be? Very challenging getting help…

Thank you again

Hello.

I know it may sound a little dumb. But I am active duty since 2019. I have contributed both 5% Trad and 5% Roth for a total of 10% of my paycheck. I just realized I have not received any match-up as you mentioned. My question is: Due to I am contributing to both systems am I automatically out of the match-up? if I am still able to get the 5% extra catch, How do I know I am receiving it?

Unless you opted out of the blended retirement you should be receiving it. They will match UP TO 5% of your base pay so as long as you contribute at least 5% they should. If you contribute 2% they’ll match that 2%. I recommend getting in contact with your branches pay/finance office.

Spencer, I can not find the answer to this anywhere. I am hoping you can help me. If I enlist today and start contributing 5%.

A. Is it 24 months until I am eligible to actually receive the matching (ie is it in an escrow type thing contributing and holding it until I am eligible at 24 months)?

B. Or is it 24 months before the government even starts matching?

Thank you

Your answer is here.

* 60 days from active duty start to start 1% matching.

* 24 months until government starts matching

There’s no escrow thing. Just set your contribution to 5% minimum, receive your 1% automatic, and then when you hit 24 months the govt 5% match will kick in automatically.

I appreciate your article – I used your percentages to max out my traditional TSP for the year.

I have a question regarding allocating bonuses to the TSP in order to get to the maximum, but also preserving the match in the final months.

I am trying to use a bonus I’ll receive later in the year to help me max out my TSP which will allow me to allocate less of my pay throughout the year. If I am going to receive a bonus of ~$4000 on September 30th and I allocate 100% of my bonuses to my traditional TSP via MyPay, will $4,000 actually get deposited in my TSP, or will taxes be taken out of the bonus first? Below are my planned monthly TSP contributions to better explain:

January: $1731.91

February: $1731.91

March – August: $1670.10 each month

September: $5836.77 (normal monthly contribution of $1670.10 + approx. bonus of $4166.67)

October-December: Allocate ~$393 each month to get to $20,500 and ensure I get my match of $309.27 each month.

My calculations only work if the full bonus will actually go into my TSP and not an unknown percentage taken for taxes. I don’t know if the military withholds the standard 22% from all bonuses, or if it makes a difference that I have bonuses allocated to TSP. I appreciate the help!

I’m not sure. Usually military bonuses are subject to tax withholding of 22%, which is usually higher than most servicemembers effective or marginal tax rate so you will get some of that back when you file your tax return.

But I could see if you are contributing the bonus to the Traditional TSP they will not withhold the 22%. If it were me, the simplest thing to do is just max out your TSP contributions with regular pay and ignore the bonus. Invest the bonus in your Roth or Traditional IRA and you will get the 22% withholding back when you file your tax return the following year.

Don’t overcomplicate something that doesn’t need to be overcomplicated. Money is fungible, so whether you invest your bonus or your monthly paycheck, you get all the same dollars in the end.

Good article and website. However, allocating TSP contributions to reach the maximum limit is often more complicated than this, as promotions and increases in YOS often come in the middle of the year, which change your base pay. I commissioned in May, so my base pay or YOS have increased in June of every year since.

To set your allocation only once at the beginning of the year, I use the following equation to determine what the single allocation percentage (X) should be:

[months at old paygrade/YOS]*[old basepay]*[X] + [months at new paygrade/YOS]*[new basepay]*[X] = [max TSP contribution limit for year]

For instance, for 2022, as O-2 with 3 YOS, set to promote to O-3 with 4 YOS at end of May:

5*$5255*X+7*$6185*X=$20500, X=0.294=29.4%

Are you sure that if your allocation is set to exceed max amount (for instance in December), the TSP will only withdraw up to the max amount? The exact wording from my November LES is “IF TSP ELECTION AMT EXCEEDS NET AMT DUE, TSP WILL NOT BE DEDUCTED.” This sounds like they would not deduct anything for the month of December if you are set to “bust”. Thus one should round allocation percentage down, not up.

Round up. Let’s take the most extreme rounding case of 0.9%. 0.9% * 11 is 9.9% extra that you’ve contributed Jan-Nov. as long as your monthly allocation to max out is greater than 15% then in December you’ll have at least 5.1% remaining and fully max out both yearly max and 5% match. Rounding down leaves you some amount short of the yearly max. Maybe not much but as you can see, there’s no reason not to round up. ;)

Spencer,

Thanks for updating the article. I may have missed this, but have you thought about adding some verbiage and a table and talking about the percentage to contribute to include “catch up contributions” for those of us that are age 50 or older? I assume BRS matches those contributions as well? Catch up contributions are again set at $6,500 in 2022. The year 2021 is the first year where you don’t have to elect the catch up contributions separately.

Thanks for all that you do.

Scott

I hadn’t thought of what Stanley69 said until I just read it but they make an excellent point unfortunately. I joined the BRS because I know I’m not doing 20 years but I THOUGHT the matching 5% would be going into my Roth TSP, not a traditional TSP. Now that I know it’s going into a Traditional TSP, I kind of want to add another 5% of my savings into my Roth TSP since that’s what I thought was happening anyway. Disheartening to say the least but Uncle Sam once again pulled the wool over my eyes.

Has their been any updates to what Jack on December 2, 2018 asked about being able to move that 5% agency match over from the predetermined automatic Traditional TSP to the Roth TSP we created? Thanks in advance!

You still get a 5% match. In the big scheme of the things, it doesn’t matter whether it goes into your Roth or Traditional TSP account. If you really want to move the needle, you should be maxing out the TSP anyways and a 5% match is just gravy. Not really sure how Uncle Sam pulled the wool over your eyes… this has been the policy since the beginning…

Because of the way TSP matches are deposited (pre-tax), they must go into the Traditional TSP, not the Roth TSP. This is standard practice in civilian 401ks with matching as well.

The BRS and TSP is still a good deal for those who don’t make it to 20 years and can be a wash vs the Legacy High 3 system for those that do make it 20 if you invest wisely.

Hey Spencer,

First off thanks for the helpful website! I am an avid follower! My question is if the TSP match from the government counts towards your annual contribution limit of 19,500?

No it doesn’t. Look at the FAQ on this page. It counts towards the “annual addition limit” of $58,000 in 2021: https://www.tsp.gov/making-contributions/contribution-limits/.

Hey Spencer,

When are you eligible for 5% matching contributions? I have been active duty for 5+ months now and am contributing much more than 5% of my base pay into my Roth TSP and have only been receiving 1% matching contributions. I have attempted to contact the TSP office multiple times regarding this issue and have not been able to get through to them. Thanks

You must complete 2 years of service before you begin receiving the 5% match. The 1% automatic contribution kicks in after 60 days of active duty service.

As far as contributing the maximum, do I need to consider how much that is being matched?

Basically, what I am asking is can I personally contribute the full $19,500 (2020) or do I need to subtract the amount that the government will be matching so my account as a whole doesn’t go over the maximum for the year? So in theory, the annual contribution to my account would then be $19.5k + (5% of my Base Pay x 12).

No, matching does not count against your elective deferral limit $19,500 in 2020. Matching is counted against the $57,000 annual addition limit. https://www.tsp.gov/PlanParticipation/EligibilityAndContributions/contributionLimits.html

For example, in 2019 the elective deferral limit was $19k and the annual addition limit $56k. (Note I rounded my contribution and matching numbers).

I contributed $11,000 to my Traditional TSP account and $8000 to my Roth TSP account. That’s $19k I contributed. The automatic 1% matching was $750 and $2995. Total deposits in my TSP for 2019 were $22,745. Very short of the TSP annual addition limit.

Great question!

Thank you for this website Spencer. I am an AF reservist and was debating on opting into the BRS. I do plan on staying in 20 years to get my 20 year letter.

What do you think about opting in with the intent of completing 20 years in the reserves OR should I just stay with the pension?

Also, I already am maxing out my Traditional TSP with my annual bonus, and my 457 via my civilian job. Do you recommend on maxing out the ROTH TSP before the Traditional TSP? I am in a high tax state (California), but I also make a lot living in San Francisco.

Thank you in advance.

If you’re going to stay in 20 years, do not opt in.

If there is even the smallest change you won’t make 20 years, opt in. You will get the matching and you still get a pension after 20 years, it’s just reduced a bit (but you got the matching along the way to make up for the reduced pension).

I opted in and here’s why.

Hey Spencer,

On the matching portion–since the matching contributions are allocated into a separate traditional TSP account, couldn’t you just move them over to your roth account once you have them? in a way, attempting to work around the bullcrap of the automatic traditional? I just opted in today…definitely waited a little longer than I needed to, but had time to think about it.

There is currently no mechanism to move Traditional TSP contributions or funds to the Roth TSP. The work around is convert the Traditional TSP to a Traditional IRA after you depart the military and then convert that Trad IRA to a Roth IRA. It’s cumbersome but can be beneficial in the right tax situation

Hopefully when the TSP implements the “TSP Modernization Act of 2017,” a law Congress passed recently, in Sep 2019 we have more options to move funds around.

Would you consider posting how you have your funds allocated?

How my funds are allocated: https://militarymoneymanual.com/asset-allocation/

You mention that you can contribute to either TSP Roth or Traditional, however I was under the impression that in order to get the 5% match, you have to contribute to the TSP Traditional? Can you clarify this?

This is incorrect. You can contribute to either Roth or Traditional and receive the match. The matching contribution funds from the government will be deposited in your Traditional TSP.

“Your Service Matching Contributions are based on the total amount of money

(traditional and Roth) that you contribute each pay period. All Service contributions

are deposited into your traditional balance.”

Page 26 of this PDF: https://militarypay.defense.gov/Portals/3/Documents/BlendedRetirementDocuments/A%20Guide%20to%20the%20Uniformed%20Services%20BRS%20December%202017.pdf?ver=2017-12-18-140805-343

Anecdotally, I have only contributed to Roth TSP this year and have received my full 5% match every month into my Trad account.

This is still a terrible deal (BRS). They are “matching” however, it’s going into traditional account (which you pay the taxes on) so is it really a 5% match when you go withdraw? Probably closer to 1-1.5%. The big gotcha is that you sacrifice a .5% multiplier by switching to (B.S. Retirement System). If you are bad with numbers and want to simplify your decision. Ask yourself is this designed to benefit me or the U.S Government? The choice should be clear. I recommend stay on the legacy system because you don’t close any doors to Guard or Reserve and the money will be far greater than the “MATCHING”.

The BRS is not a terrible deal for the majority of US servicemembers who do not make it to 20 years of service and earn the military pension. Plus, troops joining today don’t have a choice: The BRS is what you get.

With an average investment strategy earning 7% return, the BRS value can match the legacy system. More importantly, the debate when many servicemembers had the opportunity to switch into the BRS came down to freedom and choices, not the total monetary value of the pension vs matching.

Once I get on TSP.gov, where should I allocate my funds specifically? Your previous articles recommended the C fund and 1/4 of that in the S fund.

I talked about my 2018 asset allocation here but it depends on your personal situation. 4:1 C:S fund just mimics the Vanguard Total US Stock Market Fund (VTSAX or VTI).