Military Money Manual has partnered with CardRatings for our coverage of credit card products and may receive a commission from card issuers. This site may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. Some or all of the cards that appear on this site are from advertisers and may impact how and where card products appear on the site. This site does not include all card companies or all available card offers. Editorial Note: Any opinions, analyses, reviews or recommendations expressed in this article are those of the author's alone, and have not been reviewed, approved or otherwise endorsed by any card issuer. Welcome offers vary and you may not be eligible for an offer. All information about the American Express® Green Card, Marriott Bonvoy Bold® Credit Card, and the Chase Freedom Flex® Credit Card has been collected independently by Military Money Manual. These cards are no longer available through CardRatings.com. The information related to the Chase Sapphire Preferred® Card, Chase Sapphire Reserve®, United℠ Explorer Card, United Quest℠ Card, United Club℠ Card, Southwest Rapid Rewards® Priority Credit Card, Southwest Rapid Rewards® Premier Credit Card, Southwest Rapid Rewards® Plus Credit Card, The World of Hyatt Credit Card, IHG One Rewards Premier Credit Card, Marriott Bonvoy Boundless® Credit Card, and Aeroplan® World Elite Mastercard® Credit Card was collected by Military Money Manual and has not been reviewed or provided by the issuer of this product/card. These cards are also no longer available through CardRatings.com. Thank you for supporting my independent, veteran owned site.

- Budget a realistic amount for rent, food, transportation, and other expenses

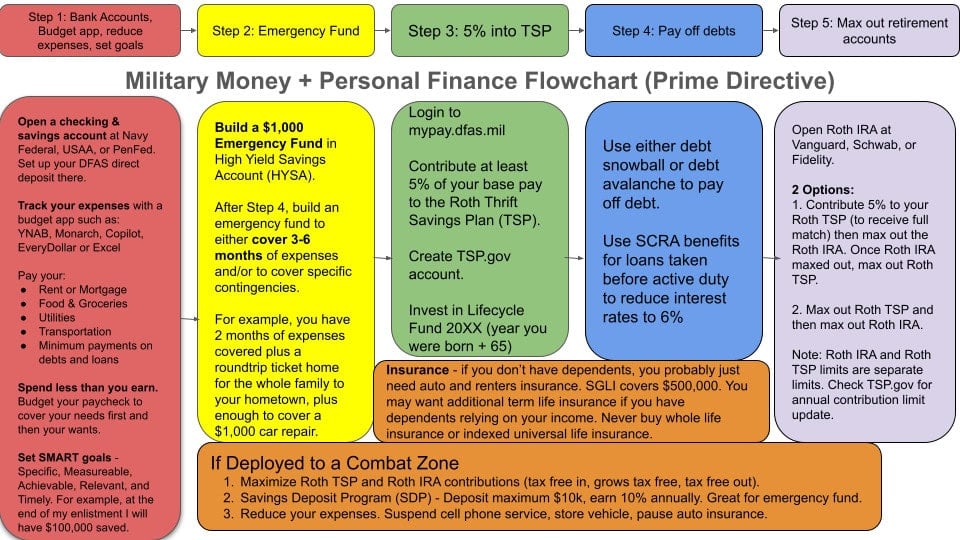

- Open a checking and savings account. USAA, Navy Federal, PenFed are popular among military servicemembers. Any bank you choose should not charge or should reimburse ATM fees. Any bank you go with should be easily used online or through an app.

- Save an emergency fund. Initially save $1000 before moving on to the next step. Then come back to this goal and save 3-6 months of expenses into a savings account. Look into High Yield Savings Accounts.

- If you are in the Blended Retirement System, start contributing at a minimum 5% into your Roth TSP account. You will get a 5% match that will go into your Traditional TSP account. This is an easy way to boost your pay by 5% per year.

- Pay down any debt you have. Use either the debt snowball or the debt avalanche technique. Whatever works for you, but get it paid off quickly.

- Max out Roth TSP. You can contribute $19,500 in 2020. If you know what an asset allocation is, feel free to set your own. While you're learning about asset allocations and growing your investing knowledge, use the furthest away Lifecyle funds. Lifecycle 2050 is my recommended fund at the moment. L2060 when that becomes available.

- Max out Roth IRA. You can contribute $6000 in 2020 in addition to the TSP limits above. Open an account at Vanguard, Fidelity or Schwab. I recommend Vanguard. Choose the further in the future Target Date Retirement Fund, like the Vanguard Target Retirement 2065.

Note if you are an O-4 or below, Roth TSP and Roth IRAs probably make the most sense for you. If your spouse works or you earn extra income from a military side business, Traditional IRAs and Traditional TSP may make more sense. Run the numbers for yourself here on the tax calculator.

Combat Zone Deployment

If you deploy to a combat zone, maximize your Roth TSP and Roth IRA contributions. Also invest the Savings Deposit Program (SDP) for a guaranteed 10% annual return on up to $10,000 invested.

The SDP is a great place to park your emergency fund while deployed.

Reduce your expenses. Suspend your cell phone service, paused your auto insurance, and reduce your fixed expenses as much as possible. My deployment savings goal was to save $50,000 on my last planned six month deployment.

Military Insurance

Never buy whole life insurance. The SGLI is $400,000 maximum for $25 per month. This is the cheapest you can find. When you deploy to a combat zone the $25 is reimbursed every month. Usually SGLI is enough until you get married or have kids. At that point look into “term life insurance.” Again, never whole life insurance. Don't mix investing with insurance. And never trust anyone from First Command.

Shop around for the best military auto insurance. GEICO and USAA tend to have very low rates and are very popular with the military. Always compare rates when you PCS. If you own a home, get home owners insurance. If you don't own a home, get renter's insurance. I use USAA for my renter's insurance.

If you find this flow chart useful, please share it on social media like Facebook, Twitter, Instagram, YouTube, Reddit, or anywhere else! You can click on the image and share it over WhatsApp, Facebook Messenger, or SMS too.

I share this flowchart with new recruits!

Thanks PAS! I hope it’s helpful.